Subordinate Debt - Discussing the Opportunities in Structured Finance

Amid rising interest rates and tightening credit markets, mezzanine debt and structured financing present compelling opportunities for investors to achieve high returns by filling gaps in the real estate capital stack while mitigating equity risk.

February 13, 2023

Introduction

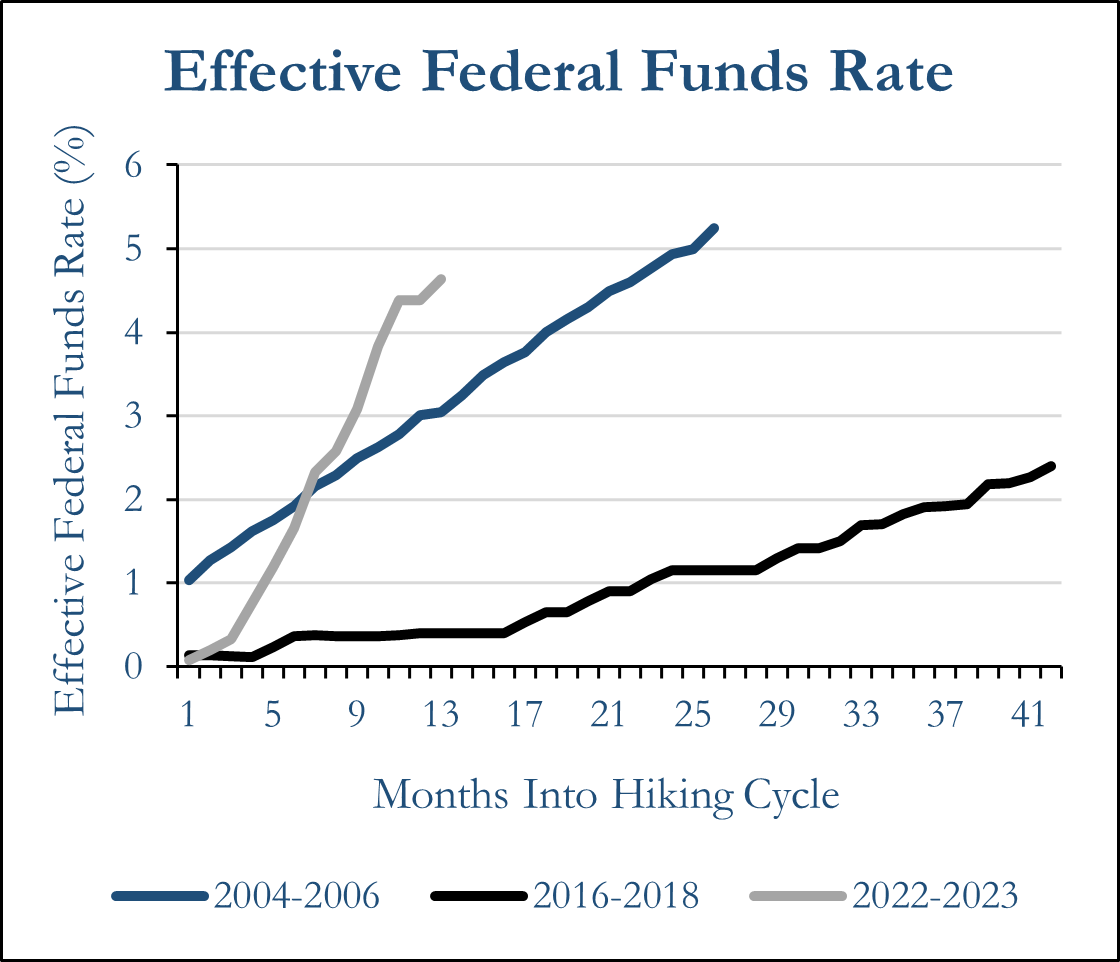

Throughout the 2010s and through mid-2022, interest rates have hovered around record low levels. Starting in January 2009, the target Federal Funds Rate dropped to zero and after being raised briefly to 2.5% after a gradual hiking cycle from 2016 to 2018, the onset of the COVID-19 pandemic dropped rates back down to effectively 0%. With the rapid rise of global inflation, central banks worldwide have taken it upon themselves to raise interest rates at record paces throughout 2022 and into 2023. Currently, the target Federal Funds Rate is at 4.25-4.50%, an increase of 425 basis points in 10 months. The steep interest rate increases by the United States Federal Reserve (“Fed”) have impacted many aspects of the U.S. and global economy and real estate is no different.

Dislocation in real estate financing has become widespread because of the increase in borrowing costs. Without sufficient NOI to cover debt costs, some owners of real estate are forced into selling their properties to relieve the burden of incurring expensive financing. Even real estate investors who have hedged interest rates are seeing distress as their interest rate caps begin to expire. In 2020-2021 when the Federal Funds Rate was essentially 0%, interest rate caps on multimillion dollar loans could be purchased for as low as $10,000. The cost to hedge the same loan today has increased tenfold [1].

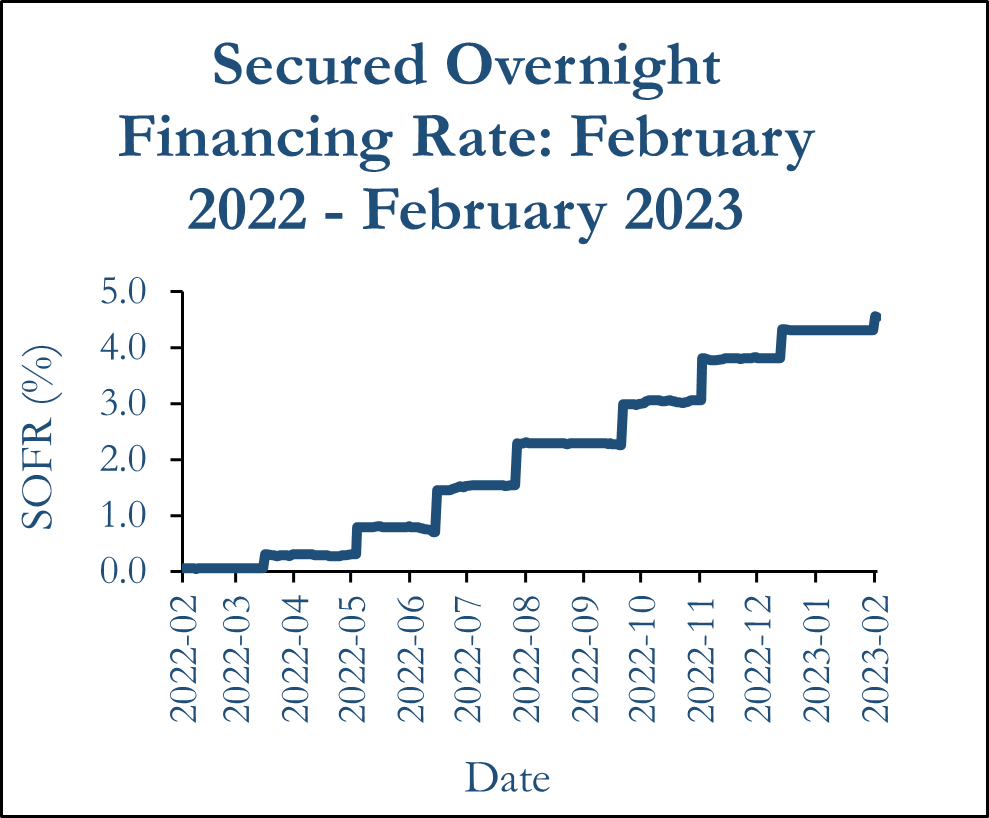

The Secured Overnight Financing Rate (“SOFR”) has increased by 425 basis points since March 2022. Source: Federal Reserve Economic Data

The Federal Funds Rate increased at the fastest pace since the beginning of the 21st century in 2022-2023. Source: Federal Reserve Economic Data

The pressures are beginning to mount on many borrowers causing considerable capital stack distress. For investors with dry powder, debt investments across the capital stack will be the most attractive option for borrowers in 2023 due to the lack of financing available from large institutions who are not willing to issue new loans. Today, ORG believes that the current environment will be the most attractive for debt investing in the past several years. ORG will discuss how structured financing can allow investors to obtain equity like returns by lending across entire capital stacks and subsequently selling senior debt while holding and collecting income from the subordinate debt.

Capital Stack Overview

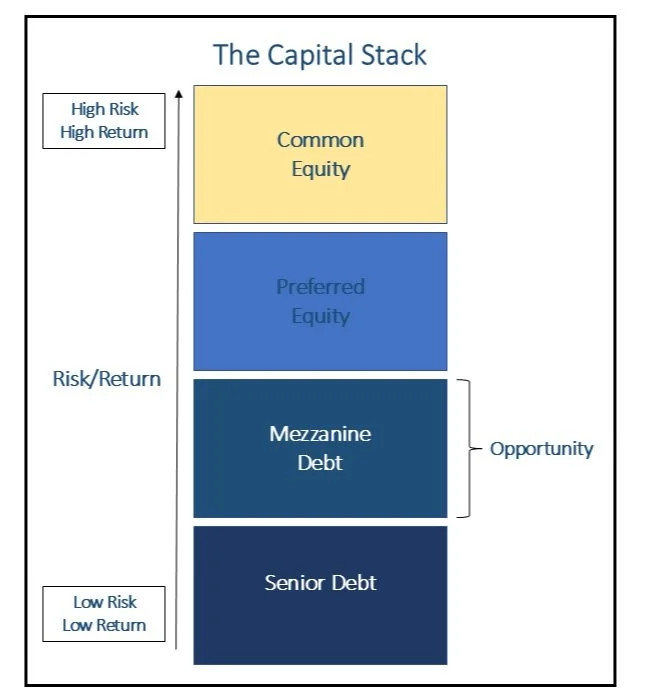

The real estate capital stack is the order in which lenders and stakeholders of any investment are prioritized when receiving cash flow from each property. Capital stacks can be made up of four separate tranches including senior debt, mezzanine debt, preferred equity and common equity.

Senior Debt

Senior debt lenders incur the least risk as they have the highest priority on cash flows produced by the investment being financed with their loan collateralized by the asset. Senior lenders’ rate of return is lower than that of the subsequent positions on the capital stack as they cannot participate in property appreciation like equity holders and receive a lower fixed interest rate than mezzanine lenders.

Mezzanine Debt

Mezzanine debt lenders are paid in subordination to senior lenders, however the interest rate they receive is higher than senior debt due to the increased risk they incur. Mezzanine debt is normally secured by ownership shares of the property as opposed to being collateralized by the property itself. [2]

Preferred Equity

Preferred equity holders can only participate in a set amount of the equity upside while having downside protection due to being prioritized over common equity holders when capital is returned. If certain defaults occur, preferred equity holders can take control of management positions but are not able to seize control of the property itself much like mezzanine debt. [3]

Common Equity

Common shareholders are those who can participate in an infinite amount of appreciation and distributions from the investment at the cost of incurring the most risk.

Capital Stack Distress in 2023

In prior years when capital markets were favorable, capital stacks could be structured with ease. Property acquisitions and developments had abundant amounts of financing options since risk assets were in such high demand. This is not the case today as dislocation in capital markets is being caused by two primary factors: cost of debt and availability of debt.

With the increases in SOFR, senior first mortgage lenders are commanding very high interest rates. This has caused borrowers to be under pressure as the cash flow from their properties may not be able to fully maintain a debt service coverage ratio (“DSCR”) that is acceptable to lenders as they look to renew debt with maturities coming soon.

This leads to the second issue of availability of senior mortgage capital. Throughout 2022 and into 2023 the amount of debt that institutional senior lenders are willing to issue has significantly decreased. In a Fed survey in October 2022, 58% of all banks stated that they have tightened their standards for commercial real estate loans with 65% of banks considered to be “large banks” tightening their standards. Over the next twelve months, 86% of all banks are expecting to tighten their commercial real estate lending standards should an economic downturn occur. [4] The tightening in bank lending standards is primarily due to the fears of increased default risk for borrowers who may be unable to service the higher costs of today’s debt, even among the most accredited institutional borrowers.

For investors today, this dislocation between reluctant senior lenders and desperate borrowers presents an opportunity for very high returning short-term mezzanine loans. In 2023 commercial mortgage originations are expected to fall to $700 billion, down 5% from the expected 2022 total of $740 billion [5] which will cause even more of a disconnect between supply and demand in the debt market. Because of this, ORG believes that in 2023, quality structured financing deals which allow for investors to lend across multiple tranches of debt, sell senior debt pieces and subsequently retain subordinate high-yielding debt will be a strategy that can generate mid-double digit returns while mitigating the risk of holding equity.

Structured Financing Opportunities in 2023

The most attractive way to invest in debt in 2023 will be holding mezzanine loans which yield high interest and have seniority to equity, however the issue with this strategy is the actual acquisition of mezzanine debt positions. Regulations will likely make it difficult to originate secondary loans on top of existing capital stacks, which is why ORG believes that structured financing is so attractive today. By issuing the entirety of the debt on a real estate asset, investors will be able to have ownership of senior debt alongside a portion of high yielding mezzanine debt. Subsequently, the senior debt can be sold off to a core focused buyer such as a commercial bank, insurance company or core real estate debt fund and the investor can maintain ownership of the mezzanine debt.

ORG believes that opportunities for high-returning mezzanine debt will arise in 2023.

With almost $175 billion in global real estate loans already in distress [6], rescue capital will be in high demand in 2023. And with many new and existing investments having loan maturities or interest rate hedges coming due this year, high credit borrowers will need new financing quickly. Therefore, they will likely need to be willing to take on higher interest debt with mezzanine pieces yielding 400-750 basis points above SOFR. Without leverage, these mezzanine loans can yield low double digit returns, and with modest leverage, investors can reasonably achieve returns in excess of 20% per year. For borrowers who secure financing in this manner, the blended all-in rate which they receive will still be favorable enough to close development deals or property acquisitions on new deals with conservative underwriting.

Conclusion

The rising interest rate environment is beginning to put large amounts of stress on real estate capital stacks today. Large institutional lenders have become more uncertain about originating new loans and will continue to grow more pessimistic throughout the year if the economy experiences a recession. Because of this, the dislocation in real estate debt markets will be significant and present lots of opportunities for debt investing. ORG believes that structured financing deals which involve originating new loans across all debt tranches and selling the senior pieces while retaining the subordinate pieces for yield will be the best way for investors to achieve high risk adjusted returns in today’s environment.

[1] Will Parker and Konrad Putzier, January 17, 2022, “Rising Interest Rates Hit Landlords Who Can’t Afford Hedging Costs,” The Wall Street Journal, https://www.wsj.com/articles/rising-interest-rates-hit-landlords-who-cant-aff ord-hedging-costs-11673900169.

[2] “The Real Estate Capital Stack: Understanding Equity vs. Debt,” ArborCrowd.com, https://www.arborcrowd.com/real-estate-investing-learning-center/capital-stack-and-equity-debt/#:~:text=The%20funds%20used%20in%20a%20real%20estate%20transaction,priority%20of%20the%20funds%20used%20in%20the%20transaction.

[3] “The Real Estate Capital Stack: Understanding Equity vs. Debt,” ArborCrowd.com, https://www.arborcrowd.com/real-estate-investing-learning-center/capital-stack-and-equity-debt/#:~:text=The%20funds%20used%20in%20a%20real%20estate%20transaction,priority%20of%20the%20funds%20used%20in%20the%20transaction.

[4] “Senior Loan Officer Opinion Survey on Bank Lending Practices at Selected Large Banks in the United States,” FederalReserve.gov, https://www.federalreserve.gov/data/documents/sloos-202210-table1.pdf.

[5] Jamie Woodwell and Reggie Booker, January 5, 2023, “MBA CREF Forecast 2023,” Mortgage Bankers Association, https://www.mba.org/news-and-research/newsroom/blog-post/mba-cref-forecast---january-2023.

[6] Neil Callanan, January 19, 2023, “Global Property Market Faces $175 Billion Debt Spiral,” Bloomberg, https://www.bloomberg.com/news/features/2023-01-20/global-real-estate-is-sitting-on-a-175-billion-debt-time-bomb?sref=t2X9isrl.