January 27, 2023

2023 United States Real Estate Outlook

Introduction

2022 was a year marked by uncertainty and volatility. For investors willing to take risks however, the year provided investment opportunities. Structural changes throughout the world in the aftermath of the COVID-19 shutdowns spurred outperformance from residential and industrial properties while punishing retail and office sectors. The high and persistent inflation which was 6.5% year-over-year in December 2022 has led investors to assess rising interest rates and the effect on the broader economy. For most of 2022, real estate professionals saw a daunting investment environment with both equity and debt capital being scarce and transaction volumes coming to a halt. This has led transaction-based valuations to become increasingly questionable.

In this article, ORG will provide insight on the key risks and opportunities facing private real estate investors in 2023.

Inflation and the Interest Rate Environment

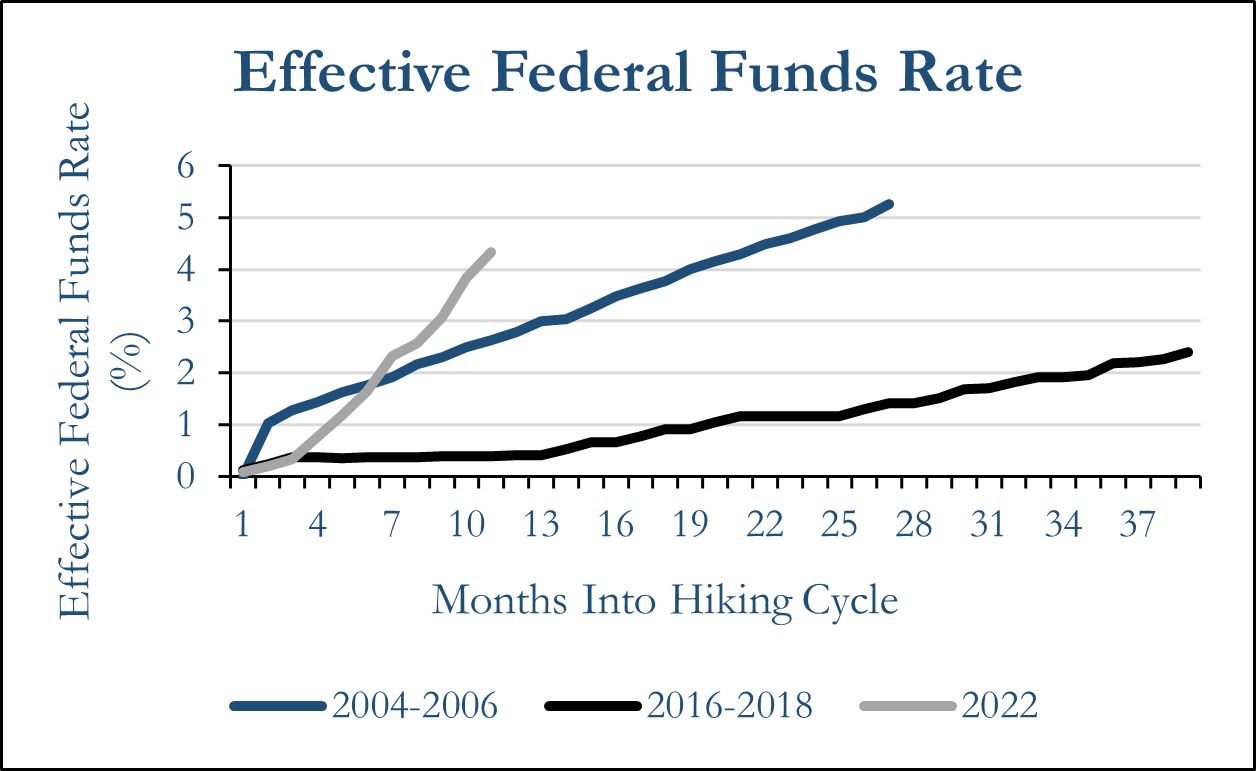

It is no secret that the Federal Reserve (“Fed”) was tough on inflation throughout 2022. Fed Chairman Jerome Powell was unapologetically hawkish in both his monetary policy actions and public remarks in an effort to break the inflation cycle which was the worst in 40+ years. During 2022, interest rates were increasing at the fastest pace since the beginning of the 21st century. Following a 25 basis point (“bp”) increase in March, a 50 bp increase in May, four consecutive 75 bp increases in June, July, September and November, the Fed increased another 50 bps in December. The target Federal Funds rate is now up 425 bps in just over nine months. In the

2004-2006 rate hiking cycle the Federal Funds rate only increased by 400 bps and in the 2016-2018 hiking cycle interest rates only increased by 225 bps. [1] This rapid shift in interest rates has shocked the capital markets as new debt adds a significantly higher cost of capital to real estate investments.

Interest Rates have increased at the fastest pace since the beginning of the 21st Century.

Source: Federal Reserve Economic Data

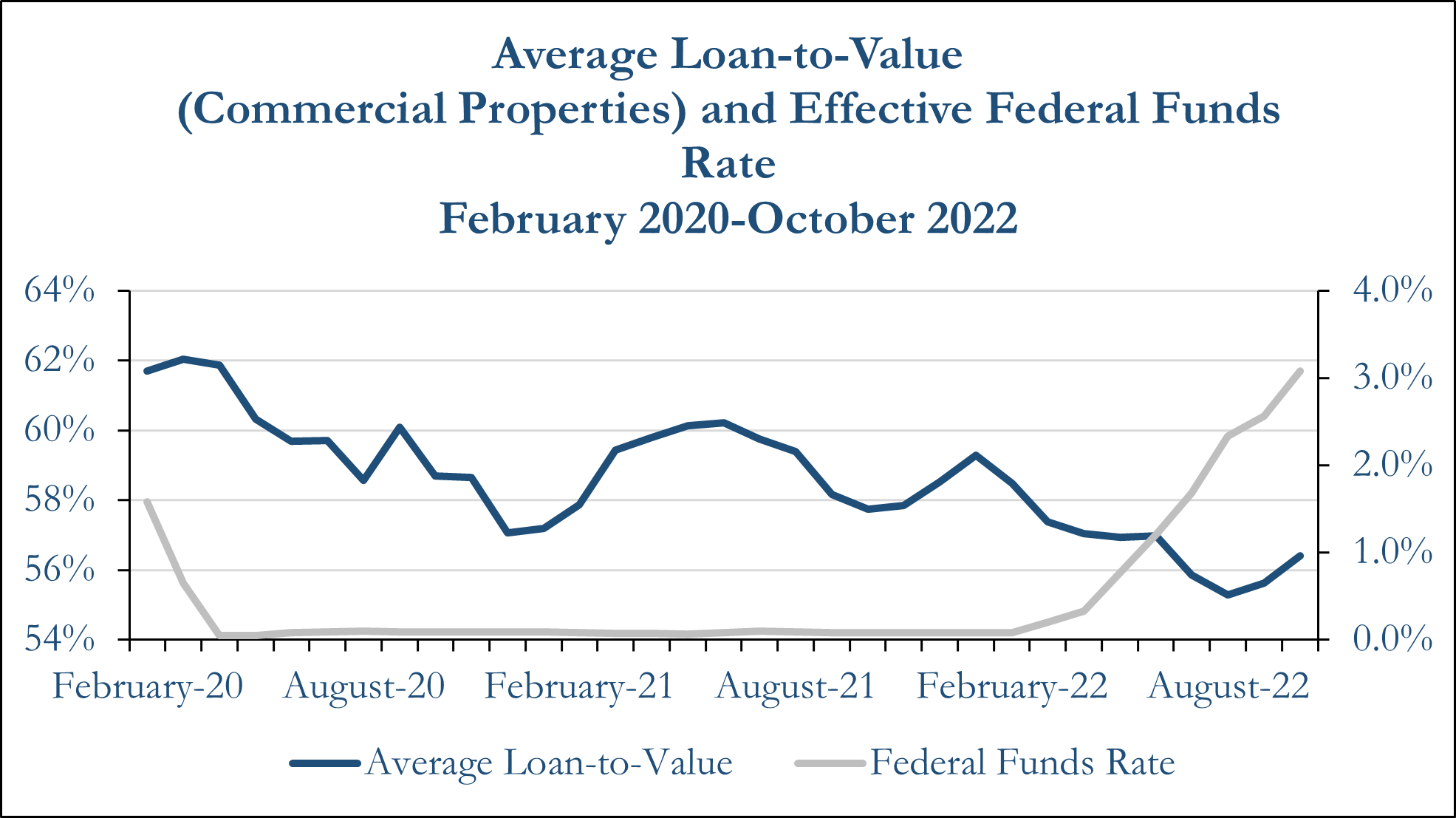

It is expected that debt market distress and dislocation will continue to rise in 2023 as lenders require higher debt yield and debt service coverage ratios (“DSCR”). Because of this change in underwriting standards, loan-to-value ratios must decrease and force borrowers to come up with more equity. Since the beginning of the pandemic, leverage ratios were already on the decline and since the inflation crisis began, they have continued to fall. The average loan-to-value on commercial properties decreased from 61.7% February 2020 to 56.4% in October 2022.

Loan-to-Value ratios have decreased as interest rates rise. Sources: Federal Reserve Economic Data, Real Capital Analytics

The increases in debt costs have not been fully realized in valuations due to lack of transactions. If NOI increases steadily and economic conditions are relatively healthy through 2023 it will offset some of the expected decreases in property valuations from cap rate expansion caused by higher capital costs. If a significant economic recession does take place as many CEOs[2][3] and economists [4] predict in 2023, NOI will shrink and fail to offset cap rate expansion.

Cap Rates and Valuations

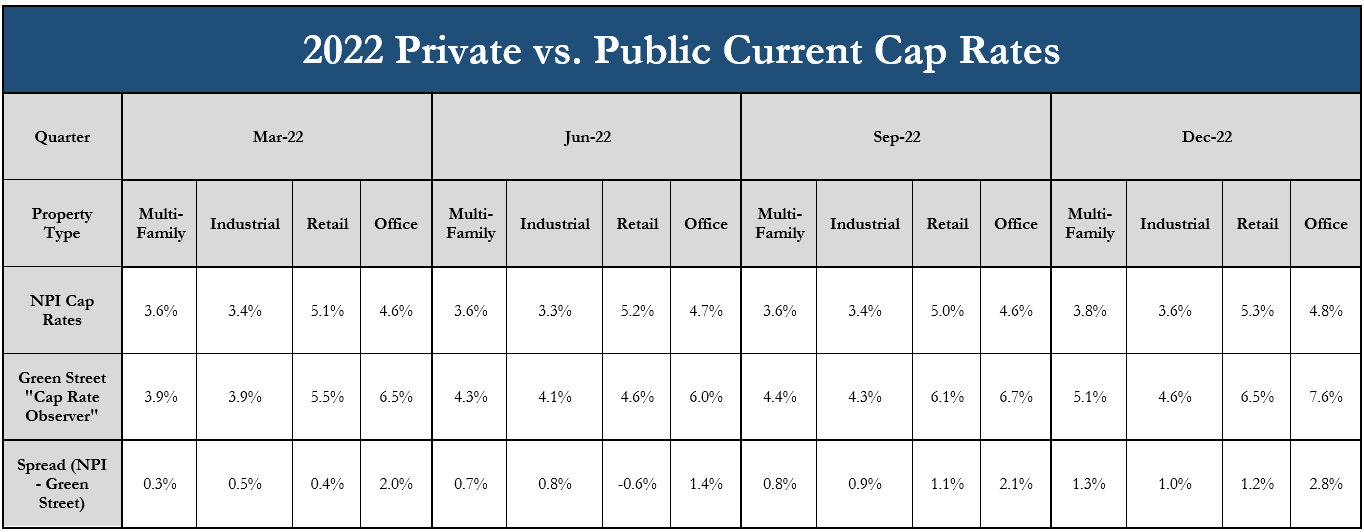

From 2020 through 2022, private real estate performed well in comparison to other asset classes. The NCREIF Property Index (“NPI”) had a one-year total return of 5.53% and a three-year total return of 8.06% for the periods ending December 31, 2022. In comparison the S&P 500 returned -18.11% over one year and 7.66% over three years ending December 31, 2022. With investor uncertainty causing a pause in real estate transactions, it is unlikely that this period of high returns will continue. A large part of these outsized returns resulted from property appreciation. Although valuations for private real estate have remained high due to lack of comparable transactions, are using public REIT valuations to forecast the direction of private real estate.[5] Using implied public REIT cap rates to forecast private real estate would indicate that private cap rates should begin to expand dramatically in 2023 as distressed sellers begin to be forced to transact. When comparing the NPI cap rates to the Green Street “Cap Rate Observer”, an aggregation of REIT cap rate data, there is a notable spread across all property types. This signals a disconnect in current private valuations and what they may look like in the future due to the macroeconomic climate.

Sources: NCREIF, Green Street

When cap rates expand from the extremely low levels as they were at in late 2021 and early 2022, property valuations will decline more than the offset provided growing NOI. With many investors seeing a substantially down year in other asset classes, they have requested redemptions from the open-end commingled funds and other private REITs to address the denominator issues plaguing their portfolios. These redemptions have caused massive redemption queues which are making liquidity an increasingly prominent issue for alternative asset managers.[6] This will further exacerbate the expected decline in overall real estate market values during 2023.

Redemption Queues, Distressed Sellers and Liquidity

Redemptions from private real estate investment vehicles such as private REITs and other private open-ended funds have been a hot topic in the media lately, however the issues of liquidity and backed up redemption queues have been a risk for many months. As institutional investors of all sizes saw significant declines in their investment portfolios throughout 2022, private real estate was one of the few bright spots of the year. As their real estate investments continued to grow in value, they needed to sell positions in real estate and reallocate their portfolio to public equities and venture capital due to the denominator effect. [7]

Blackstone Sold its 49.9% stake in the Mandalay Bay and MGM Grand hotels to Vici Properties. The deal is expected to return a profit of over $700 million to Blackstone which they will use to help pay out redemption requests from BREIT. Source: The Wall Street Journal

This trend has caused many real estate investment managers to limit investor withdrawals and scramble to raise liquidity to pay out redemption queues. To satisfy this, managers are looking to sell their premier income-producing assets quickly to raise as much cash as possible and pay out their queues.[8] If cap rates continue to expand in the private markets, some managers may be forced to sell assets at a significant discount to their all-time highs to raise liquidity this year.

Investment managers are not alone in looking for liquidity. The institutional investors who are requesting redemptions from the open-end funds also have a significant need for cash to pay their beneficiaries while their fund balances were crushed by negative returns in fixed income, public equities and venture capital throughout 2022. To fund distributions, many are looking to sell their positions in closed-end funds on the secondary markets at a significant discount to net asset value which would present a potentially attractive opportunity for investors who are comfortable with lower liquidity in the short term.

Opportunities

Rising interest rates coupled with expanding cap rates, ballooning redemption queues from open-ended funds and low liquidity will most likely be the cause for headwinds in private real estate returns in 2023. Despite this, ORG believes that the potential short-term distress in private real estate in 2023 will reward long-term investors who can properly manage risk and source quality opportunities. ORG’s outlook on each of the major property types are as follows:

Industrial

The growth of e-commerce has made industrial the sector of choice for most investors since the beginning of the COVID-19 pandemic. Industrial market rental rates have increased by double digit percentages year-over-year from 2020-2022 as supply chains became stressed and logistics tenants were willing to pay a premium to expand their e-commerce logistics network. As the supply chains worldwide begin to ease, ORG sees this trend slowing significantly as the sector has grown overcrowded.

The best opportunities for industrial in 2023 reside in acquisitions of assets which are well located around infill locations. These assets have significant barriers to entry since vacant land is very expensive, in limited supply and difficult to develop as many cities are now limiting additional zoning for new industrial development. The spreads between market value of property acquisitions and replacement cost are still attractive in many cases allowing for investors to enter at a relatively attractive basis. Infill industrial acquisitions are also ideal since these properties will be able to limit obsolescence risk from assets located too far from the consumer market. ORG believes that industrial assets located outside of city centers do not hold as much value as infill industrial in the long term and that they will be priced at a significant discount to replacement cost in comparison to infill locations.

Multifamily

Multifamily was another outperforming sector through 2022 and is also likely too saturated for further investment. Rent growth has slowed since the middle of the year and an overall stagnation of the economy could signal some slowing in rental absorption. Despite this, ORG believes that the rise in mortgage rates combined with an overall shortage of housing units in the United States will keep renters in the market.

ORG believes that core property acquisitions in gateway markets with high barriers to entry will continue to see occupancy and rent growth in 2023. Relatively high home prices coupled with mortgage rates that have essentially doubled in the past 12 months will deter potential homebuyers from their searches and prevent current homeowners who were considering moving from selling. This will lead to individuals currently renting to continue doing so for longer. For investors looking for opportunistic returns in multifamily, workforce housing development opportunities will continue to exist in non-gateway cities experiencing high job and population growth where barriers for new development are low and existing workforce housing stock is limited.

Retail

Retail has been a sector shrouded in uncertainty as the effects of COVID-19 causing a rise in the popularity of e-commerce decreased its performance. Over the past three years, malls and other retail assets targeting discretionary consumer expenditure have performed rather poorly while grocery anchored retail has remained steady with the demand for need-based products and services.

ORG sees the conservative strategy for traditional grocery anchored retail to generate solid returns throughout 2023 but the more specialized ethnic grocery anchored retail will likely see notable outperformance to traditional grocers in the new year. Changing demographics in United States growth markets, including a 20.8% increase in Hispanic-Americans and a 29.6% increase in Asian-Americans from 2011 to 2021[9], make this area increasingly more attractive for both core investments and non-core development strategies.

Office

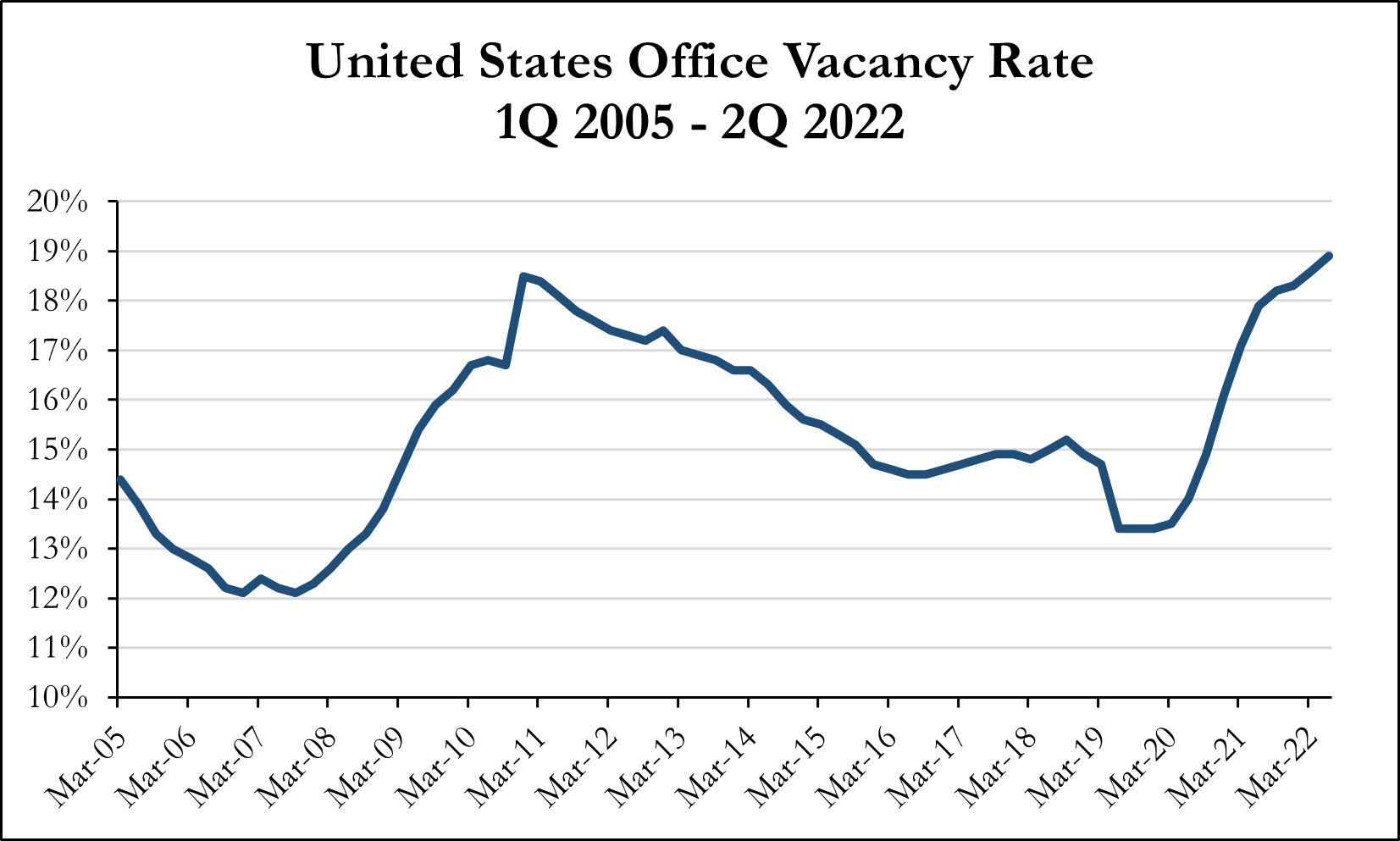

It is no secret that traditional office investments have been negatively affected by the COVID-19 pandemic. Work-from-home trends have decreased occupancy, and meanwhile physical occupancy, or the number of workers who actually are present in the office on a day-to-day basis, has fallen even further. Companies beginning to require their employees to return to work may seem to be a potential tailwind for the sector, however many investors overlook the fact that the oversupply of office began decades before the pandemic. Tax incentives, particularly in the 1980s and early 2000s stimulated rapid and excess development of central business district office supply and pre-pandemic vacancy of office remained in the double digits as a result.[10] For these reasons, ORG still is skeptical on traditional office in 2023. Although Class-A office with new and exciting amenities may entice some of the labor force back to in-person work, ORG expects these investments to incur excess risk.

Office vacancy in the United States has remained high since the mid-2000s. Source: JLL

ORG believes that even life science which has been a hot sector throughout the COVID-19 pandemic faces significant headwinds in the coming months. With the slowing economic environment, total venture capital funding fell by 37% in 2022[11]. This is concerning as many early to mid-stage life science companies rely on consistent venture funding in order to operate their businesses. This decrease in capital funding for the industry could lead to slowing tenant demand and significant value capitulation.

The office sector is not completely barren of opportunity as medical office has grown to become an attractive alternative to traditional office. Core medical office leased to quality tenants has inelastic demand and sticky tenants which present attractive opportunities for larger income returns. Over the long-term, medical office could also outperform as the United States population continues to age and require more regular medical care. As of July 2021, the population of US seniors (60 years or older) was 77.1 million with an additional 21.2 million Americans expected to become seniors by 2026.[12] This trend could lead to increased demand for healthcare services and medical office space.

Other

ORG suggests that investors pay attention to the hotel sector in 2023. Although business travel has struggled to return to pre-pandemic form, leisure travel has been very strong since travel bans and pandemic lockdowns have been lifted. ORG believes that while a deep recession in 2023 would be troublesome for hospitality, in a soft-landing or mild downturn scenario, business and leisure travel will both continue to recover considerably leading to hotel outperformance.

Whether or not investors allocate capital to hotels, it is worth paying attention to how hotel occupancy and rental rates behave throughout 2023 as hotel demand can often be a leading indicator of what is to come in the broader economy.

Conclusion

ORG believes that asset repricing and global transitioning back into the pre-pandemic way of life will mark significant changes in real estate in 2023. The effects of interest rates on financing costs will decrease asset valuations. ORG believes that this anticipated shake-up in prices will provide ample opportunity for prudent investors to acquire high-quality assets at significant discounts. Additionally, ORG believes that institutional investors should ensure that their portfolios are allocated with high conviction investment managers who have proper alignment of interests in order to reduce risk in a potential low-returning environment.

[1] Taylor Tepper, November 2, 2022, “Federal Funds Rate History 1990 to 2022,” Forbes Advisor, https://www.forbes.com/advisor/investing/fed-funds-rate-history/.

[2] Hugh Son, December 6, 2022 “Jamie Dimon says inflation eroding consumer wealth may cause recession next year,” CNBC, https://www.cnbc.com/2022/12/06/jamie-dimon-says-inflation-eroding-consumer-wealth-may-cause-recession-next-year.html.

[3] AnnaMaria Andriotis, December 6, 2022 “Goldman CEO David Solomon Prepares for a Possible Recession,” The Wall Street Journal, https://www.wsj.com/articles/goldman-ceo-david-solomon-prepares-for-a-possible-recession-11670357873?mod=Searchresults_pos5&page=1.

[4] James Mackintosh, December 4, 2022 “Economists Think They Can See Recession Coming – for a Change,” The Wall Street Journal, https://www.wsj.com/articles/economists-think-they-can-see-recession-comingfor-a-change-11670150634?mod=Searchresults_pos1&page=1.

[5] Loretta Clodfelter, June 1, 2018, “Leading Indicators: REITs may provide insight into private real estate pricing,” IREI, https://irei.com/publications/article/leading-indicators-reits-may-provide-insights-private-real-estate-pricing/.

[6] Mark Heschmeyer, December 5, 2022, “Starwood, Other REITs Join Blackstone in Limiting Investor Withdrawals As Economic Concern Spreads,” CoStar News, https://product.costar.com/home/news/954216073.

[7] Erik Sherman, December 2, 2022, “Institutional Investors May See Too Much Investment in CRE,” Globest.com, https://www.globest.com/2022/12/02/institutional-investors-may-see-too-much-investment-in-cre/.

[8] Peter Grant and Miriam Gottfried, December 1, 2022 “Blackstone Stake Sale Values MGM Grand, Mandalay Bay at $5.5 Billion,” The Wall Street Journal, https://www.wsj.com/articles/blackstone-stake-sale-values-mgm-grand-mandalay-bay-at-5-5-billion-11669880302?mod=Searchresults_pos2&page=1.

[9] USA Facts, 2022, “Our Changing Population: United States,” usafacts.org, usafacts.org/data/topics/people-society/population-and-demographics/our-changing-population?endDate=2021-01-01&startDate=2011-01-01.

[10] Konrad Putzier, August 23, 2022 “America’s Office Glut Started Decades Before Pandemic,” The Wall Street Journal, https://www.wsj.com/articles/americas-office-glut-started-decades-before-pandemic-11661210031.

[11] January 11, 2022 “State of Venture 2022 Report,” CB Insights, https://www.cbinsights.com/research/report/venture-trends-2022/

[12] “Population of the US by sex and age as of July 1, 2021,” Statista, https://www.statista.com/statistics/241488/population-of-the-us-by-sex-and-age/