April 2, 2023

Single Family Rental Homes:

The Cutting-Edge of Residential Real Estate Investing

Introduction

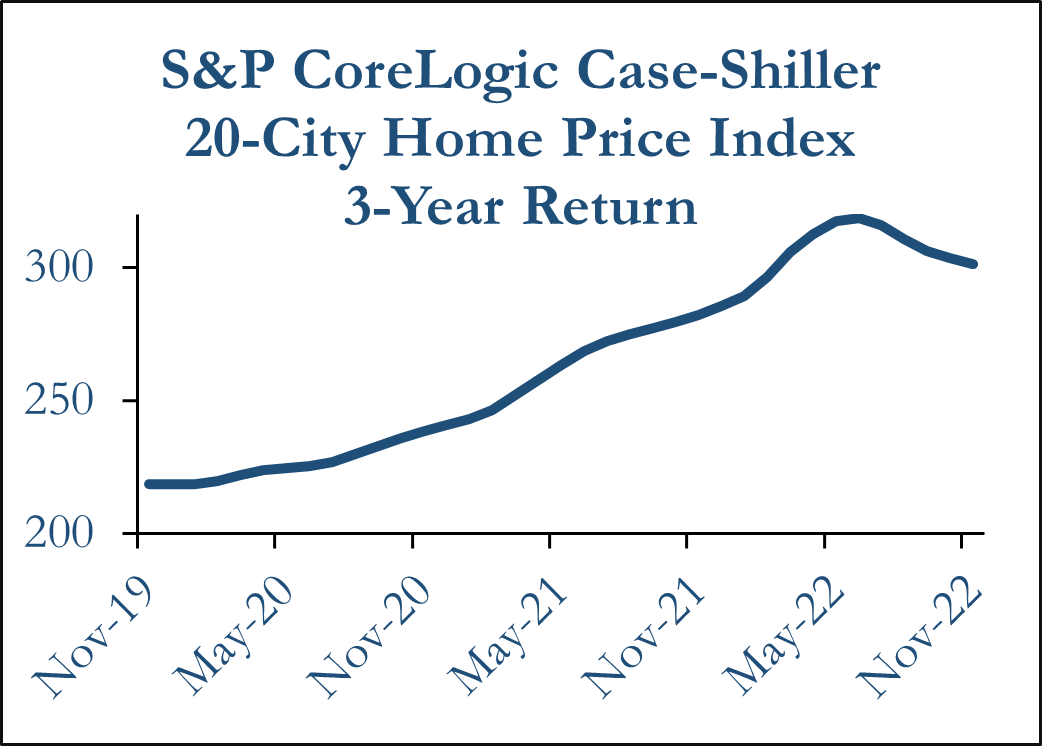

Recently, housing affordability has been a topic at the forefront of the real estate industry in the United States. Due to stagnant inflation adjusted wages and increasing mortgage rates eclipsing 20-year peaks of nearly 7% [1], homeownership is more difficult than ever for the average American family. As a result, the number of homeowners has declined steadily since the mid 2000’s and was further accelerated by the Global Financial Crisis. According to the S&P CoreLogic Case-Shiller 20-City home price index, homes were 6.77% more expensive year-over-year from November 2021 to November 2022.

As housing affordability conditions continue to worsen, the spread between the cost to rent and the cost to own has widened quickly. As of June 2022, the monthly cost of a mortgage payment was over $800 higher per month than a rental payment on a similar space. This is the highest mortgage-lease spread since the beginning of the 2000’s [2].

As a result of these market conditions, rental housing has become far more attractive and cost effective for most individuals. Today, the Single-Family Rental (“SFR”) market has exploded in popularity among both Americans looking for affordable housing options and real estate investors alike.

The value of the Index increased at an 11.31% annual rate from November 2019 to November 2022. Index values as of February 2023. Source: S&P Dow Jones Indices

The History of Single-Family Rentals

Historically, SFRs have been largely owned and operated by mom-and-pop investors and only recently been considered a viable asset class for institutional investors. SFRs first became popular for institutions in late 2008 and early 2009 after the Global Financial Crisis (“GFC”) caused a dramatic drop in home prices, which were down by an average of 20.6% from their highs in July 2006 to their lows in March 2009 [3]. A combination of foreclosures on homes with subprime mortgages and real estate investors who saw the discounted prices as a buying opportunity caused many homes to change hands from individuals to institutions. Since the GFC, rental homes have grown in popularity for Americans seeking housing options and real estate investors.

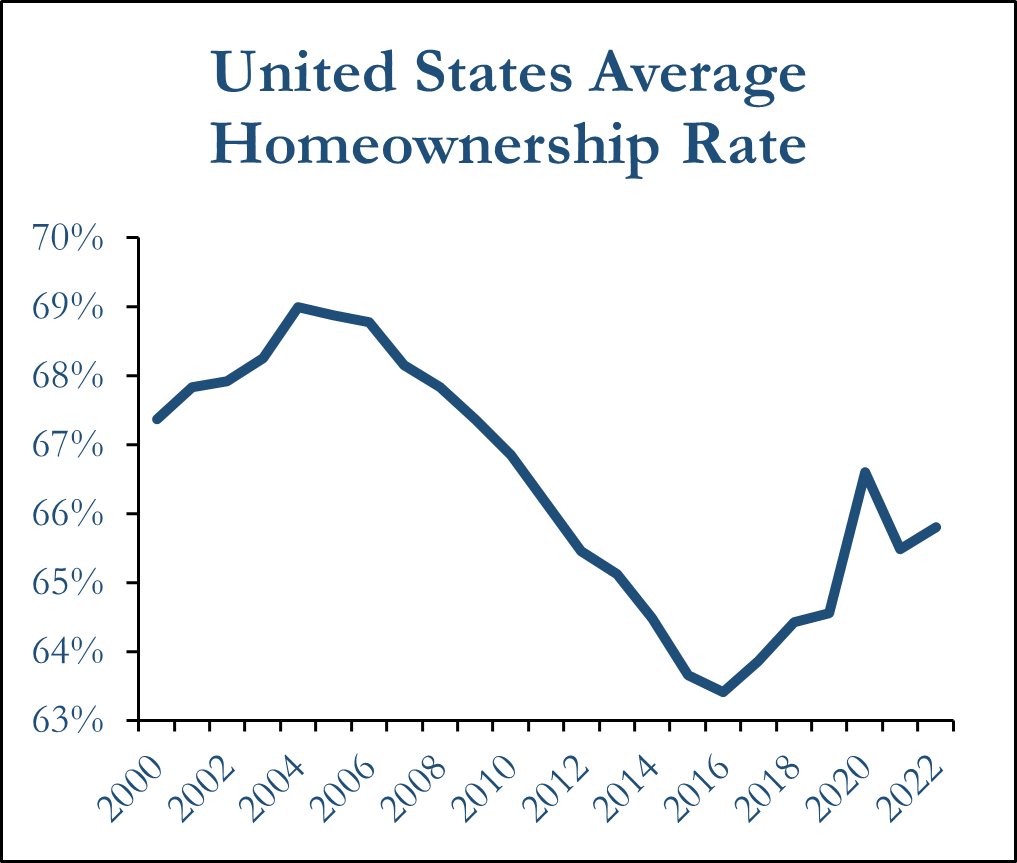

The Homeownership Rate in the United States has decreased on average since 2004. Source: Federal reserve Economic Data

Today, the U.S. Millennial generation (born between 1981 and 1996) with a total population of over 72 million are reaching their prime homeownership years. At first glance, this would lead many to believe that rental rates are on the decline. Instead, Millennials and Gen-Zs (born between 1997 and 2012) who live on their own decide to rent at a significantly higher rate than preceding generations due to slow real wage growth, rapidly declining affordability of homeownership and monthly expenses such as food and utilities at all-time highs. This issue is further exacerbated by student loan debt which is a common burden for most Millennials and Gen-Zs. Now homeownership is significantly below its 2004 high of 69.0% and was at 65.5% in 2021 following a 50-year low of 63.4% in 2016. These lower numbers are primarily dragged down by the cost conscious preferences of Millennials and Gen-Zs [4]. Despite lower homeownership, Millennials and Gen-Zs still want the square footage and welcoming home-like feeling that SFRs offer which has led to a large demographic shift in demand for this specific asset class.

Source: Green Street U.S Single-Family Rental Outlook

Demographic Shifts Effecting Residential Real Estate

Demographic changes in the U.S. can be seen as a major contributing factor to the rise in SFR popularity as the increase in Millennial and Gen-Z renters has spurred a new era where SFRs are preferable to homeownership and apartment rentals. As Millennials age and start families of their own, they want more housing space, yard space and a neighborhood community without the cost burden of a mortgage. With SFRs, renters can live in a home while having the flexibility to take on a new employment opportunity in a different location without the stress that comes with selling their current home. In addition, they can have the space and access to neighborhoods and school districts which an apartment rental may be unable to provide.

A Lease-Purchase agreement is a structured rent contract which has grown in popularity since it allows Millennial and Gen-Z renters who would eventually like to become homeowners to work toward homeownership more gradually. These contracts allow a potential homebuyer to rent a home for some time before purchasing the property from the landlord/seller at an agreed upon price. The rent for these homes is higher than the fair market price and the increased cost doubles as a contribution for the eventual down payment on the home [5]. The Lease-Purchase model can be favorable for younger professionals who are looking to own but may not have the cash on hand to place a down payment. With a Lease-Purchase agreement, they can build equity in a down payment slowly and have flexibility if they decide not to own.

Whether these young renters decide to own, rent or Lease-Purchase, location, size and amenities are the main drivers that cause Millennials and Gen-Zs to choose what kind of SFRs they want to occupy. SFRs come in many variations with the two main types being Scattered Site homes and Build-For-Rent housing.

Single-Family Rental Investment Strategies

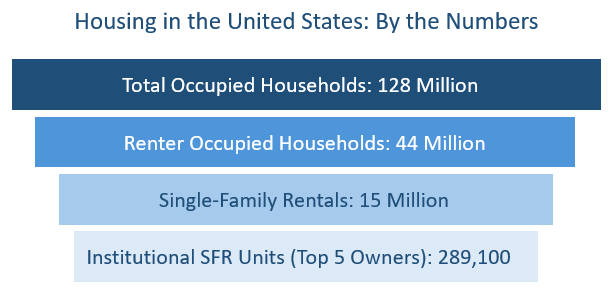

Scattered Site and Build-For-Rent strategies both have different characteristics which can make one or the other appear more favorable to each investor. Scattered Site rental strategies are executed through the acquisition and aggregation of multiple rental properties which were pre-built single-family homes and are often not located in the same development or residential market. The Build-For-Rent (“BFR”) housing strategy consists of the construction and leasing of multiple properties in the same development. BFR homes are constructed exclusively for the purpose of lease up and can be thought of as “horizontal multifamily” residential living. BFR communities will often have amenities similar to apartment complexes such as pools, playgrounds and dog parks [6]. As both investment strategies have become more popular, the United States has seen a significant increase in the number of renters with 44 million households, including both single and multifamily housing, are being renter-occupied [7]. SFR homes make up about 15 million of the total as of 2020 [8].

A Build-For-Rent Community with Amenities

Scattered Site

Scattered Site SFR investing consists of picking and choosing individual properties or small portfolios of SFR units that are not adjacent to each other and can often be situated in different neighborhoods, submarkets, or even regions. Historically, homes which end up becoming Scattered Site portfolio properties for institutional investors often are purchased through the foreclosure process. Banks who foreclose on these properties find that they are in significant need of repositioning which some investors see as an opportunity to purchase residential units at a discount. Some of the homes which are acquired through the Scattered Site strategy may be operated on a lease-purchase model, but the majority will end up being leased long term [9].

Today, Scattered Site investing has evolved and become more efficient for institutional investors. Many firms now use data-driven solutions for property searches and purchases. Advanced algorithms now allow Institutions to search Multiple Listing Service (“MLS”) databases quickly and bid on single-family properties from across the country without direct oversight or significant submarket knowledge [10].

Scattered Site housing often becomes institutionalized after being foreclosed upon and is in need of repositioning.

Expenses for large Scattered Site portfolios tend to be rather high due to efficiencies of scale being limited by the spread-out ownership style. Many services involved with property management become more difficult when properties are spread out rather than being within the same community [11]. While property management and repositioning costs may reduce overall returns, investors can find some solace in the broad spectrum of possible exit strategies of this asset class. Common exit strategies from Scattered Site SFRs are usually full portfolio sales or dispositions of only a handful of properties to regional or local buyers in some niche instances.

Some investors may be deterred from the irregularities which may arise from a Scattered Site strategy, and for them Build-For-Rent investing may be more fitting for their investment strategy.

Build-For-Rent

BFR housing is a strategy in which a property or community is developed from the ground up with the sole purpose of being rented. BFR housing is commonly seen in the United States as attached housing or townhomes as well as fully planned neighborhoods which contain standalone houses. These units are all developed in a single project allowing for uniformity in structure, appearance, square footage and interior appliances. This uniformity and proximity of the units can make property management far easier especially with new home rental software making payment processing and maintenance requests quicker and more efficient.

Demand for BFR housing has been extremely strong and approximately 2.5 million additional BFR units within the next decade would be needed to satisfy that demand. Homebuilders are increasingly becoming more receptive to developing BFR housing as opposed to traditional single-family housing however the lack of a robust development pipeline that can keep up with growth in housing demand may likely lead to shortages well into the future [12].

The popularity of BFR housing in institutional real estate investing is quickly growing. The total amount of BFRs as a percentage of all Single-Family home starts reached an all-time high volume of 6.3% in 4Q 2022, compared less than 3% following the Global Financial Crisis [13].

Due to the favorable growth fundamentals, market drivers and stable returns, investors are in discussions with managers to add SFRs to their portfolio which has led to the increase in the production of BFRs.

Single-Family Rental Market Analysis

With the significant demand for both Scattered Site and Build-For-Rent housing, occupancy for the asset class was 94.6% in 4Q 2022. Many investors have seen significant interest in markets with high job growth and population growth such as emerging cities in Alabama, Tennessee and the Carolinas [14]. Other markets with high income and population growth such as Florida, Georgia and Texas also have significant demand for SFRs.

Valuations and rent growth have steadily increased over time and capitalization rates (“cap rates”) for SFRs were 5.6% in 4Q 2022 which was slightly higher than their all-time lows in 2021 but still extremely low compared to the pre-COVID cap rates of well over 6%. The cap rate spread over 10-year Treasury yields for the fourth quarter of 2022 was 181 basis points reflecting a narrowing risk premium which is primarily being influenced by the rapid increase of Treasuries. The SFR-Multifamily cap rate spread was 87 basis points in 4Q 2022, revealing that the two property types are getting closer to parity. The improvements in SFR yields can largely be attributed to management becoming more efficient with improvements in communication technology and automation of payment processing [15].

SFR REITs have seen excellent growth as of late despite declines in share prices. Two of the largest public SFR owner-operator REITs, Invitation Homes (NYSE: INVH) [16] and American Homes 4 Rent (NYSE: AMH) [17], both recorded 9.1% in NOI growth for full year 2022. Both operators foresee higher expenses and slowing NOI growth for 2023 but AMH and INVH still forecast 3%-5% and 4%-5.5% NOI growth respectively in their full year 2023 guidance [18].

Conclusion

ORG believes that SFRs are a dynamic extension of the traditional residential market that can be seen as a replicable strategy and an area of outperformance in today’s real estate market. Strong demand for renting across multiple generations in the United States along with other demand drivers which increase the population of renters have made the asset class very viable in the market today.

Increased capital flow into the sector has not yet translated to large-scale institutional interest as institutional investment capital is still a fraction of the total SFR market. While it has increased significantly since the 2000’s, the total market share of the top five institutional SFR owners is only 2% of all SFRs in the market today [19].

As SFR ownership has grown more popular, it has also become a hot topic in the national media as being a negative for the average individual looking to buy a home. Activists often criticize investors flush with cash for purchasing homes that they themselves will not end up occupying and actively contributing to the housing affordability crisis. While ORG does acknowledge and understand this criticism (particularly for Scattered Site investing), institutionalized SFR ownership can be a powerful and positive force in fighting the United States housing crisis with Build-For-Rent home development increasing the supply of housing and in turn causing housing to be more attainable and affordable for all Americans.

Simultaneous NOI growth and cap rate compression have caused investors to take notice of SFRs and development or acquisition in strong growth markets are worth consideration. Both the Scattered Site and BFR approach to development, lease-up and operation can be seen as viable strategies. ORG believes SFRs are a prolific asset class and can provide increased diversification within residential real estate portfolios.

[1] Ben Eisen, October 13, 2022, “Mortgage Rates hit 6.92%, a 20-Year High,” Wall Street Journal, https://www.wsj.com/articles/mortgage-rates-hit-6-92-a-20-year-high-11665669624?mod=Searchresults_pos1&page=1.

[2] Danielle Nguyen, June 10, 2022, “The Light: Demand Shifting from Owning to Renting” John Burns Real estate Consulting, https://www.realestateconsulting.com/demand-shifting-from-owning-to-renting/.

[3] St. Louis Fed, “S&P/Case-Shiller U.S. National Home Price Index,” fred.stlouisfed.org, https://fred.stlouisfed.org/series/CSUSHPINSA.

[4] Mortgage News Daily, “Homeownership Rate,” https://www.mortgagenewsdaily.com/data/home-ownership#about.

[5] ”Lease Purchase Agreement” ContractsCounsel, https://www.contractscounsel.com/t/us/lease-purchase-agreement.

[6] Than Merrill, 2022, “Build-To-Rent (BTR): The Housing Trend You Should Invest In,” FortuneBuilders.com, https://www.fortunebuilders.com/build-to-rent/.

[7] John Pawlowski et al., January 25, 2023, “U.S. Single-Family Rental Outlook,” Green Street.

[8] John Pawlowski et al., January 25, 2023, “U.S. Single-Family Rental Outlook,” Green Street.

[9] Kat Aaron, April 25, 2012, “Tackling the Challenge of Scattered Site Rentals” , ShelterForce.org https://shelterforce.org/2012/04/25/tackling_the_challenge_of_scattered-site_rentals.

[10] June 2, 2021 “Invesco-Backed Mynd to spend $5B on single-family rentals”, The Real Deal, https://therealdeal.com/2021/06/02/invesco-backed-mynd-to-spend-5b-on-single-family-rentals/.

[11] Kat Aaron, April 25, 2012, “Tackling the Challenge of Scattered Site Rentals” , ShelterForce.org https://shelterforce.org/2012/04/25/tackling_the_challenge_of_scattered-site_rentals.

[12] Todd LaRue, “Build-To-Rent: The Single-Family Rental Boom”, RCLCO, https://www.rclco.com/wp-content/uploads/2021/12/Advisory-BFR-SFR-Research-Presentation-Slides.pdf.

[13] 2022, ”Single-Family Rental Investment Trends Report 4Q 2022” Arbor.com https://arbor.com/research/single-family-rental-investment-trends-report-q4-2022/.

[14] 2022, ”Single-Family Rental Investment Trends Report 4Q 2022” Arbor.com https://arbor.com/research/single-family-rental-investment-trends-report-q4-2022/.

[15] 2023, ”Single-Family Rental Investment Trends Report 4Q 2022” Arbor.com https://arbor.com/research/single-family-rental-investment-trends-report-q4-2022/.

[16]February 15, 2022, “Invitation Homes Reports Fourth Quarter 2022 and Full Year 2022 Results” Invitation Homes, https://www.invh.com/news-events/news/news-details/2023/Invitation-Homes-Reports-Fourth-Quarter-2022-and-Full-Year-2022-Results/default.aspx.

[17] February 23, 2022, “American Homes 4 Rent Q4 2022 Earnings Call Transcript” Yahoo Finance, https://finance.yahoo.com/news/american-homes-4-rent-nyse-172358969.html.

[18] John Pawlowski, Alan Peterson, February 23, 2022, “American Homes 4 Rent: Taking Longer to Scale” Green Street.

[19] John Pawlowski et al., January 25, 2023, “U.S. Single-Family Rental Outlook,” Green Street.

A Build-For-Rent community with a uniform design can streamline property management.