November 14, 2023

Property Assessed Clean Energy Loans:

An Alternative Financing Solution in a Tight Lending Environment

Introduction

Since the United States Federal Reserve began its monetary policy tightening cycle in March 2022, the benchmark interest rate increased from 0%-0.25% to 5.25%-5.50%. This increase in financing costs has sent reverberations throughout the ecosystem of commercial real estate by decreasing the availability of financing from commercial banks and slowing real estate transaction volumes and construction activity. As a result, many real estate developers have been stuck in an unfortunate circumstance where capital market conditions have restricted the viability of new construction and asset repositioning.

In order to finance construction opportunities in real estate, a growing number of investors and developers are beginning to look to Property Assessed Clean Energy (“PACE”) loans in the absence of affordable financing in the market. In this article, ORG will briefly address what PACE loans are, how to qualify for and secure PACE financing and how PACE financing can improve capital structures for investors looking to complete real estate investments that have experienced issues with rising financing costs.

What Are PACE Loans?

PACE loans are non-recourse, assumable, fixed rate financing instruments that are issued to real estate developers and individuals to make energy efficiency improvements to their assets. PACE loans are split into two different variations, Residential PACE (“R-PACE”) loans that are used for individuals to make energy improvements to their homes and Commercial PACE (“C-PACE”) loans that are used for commercial real estate investment into construction of or improvements into institutional quality properties. Real estate projects can qualify for C-PACE financing if they are used primarily for renovations or additions that improve the energy efficiency of a building. Some of the improvements that can qualify for C-PACE financing include renewable energy generation such as solar, wind or hydroelectric power generation, green roofs, water efficient plumbing, energy efficient HVAC, building insulation, efficient lighting, high-efficiency windows and elevator updates [1]. In most cases, C-PACE loans can be used to cover 100% of the costs of these renovations, which may lead them to be a significant portion of the capital stack on a project. C-PACE loans are structured as a tax assessment on a property which is paid based on the useful life of the energy efficient improvements being made [2]. C-PACE loans also cannot be accelerated or prepaid.

The principal balance of a C-PACE loan is subordinate to senior financing. Due to its structure as an assessment however, the periodic C-PACE payments have priority over the payment to the senior lender. Because of the unique structure, senior lenders must give their consent for a borrower to secure C-PACE financing on an asset [3]. Additionally, C-PACE financing does not affect the ability of the senior lender to foreclose on an asset because it is structured as an assessment [4].

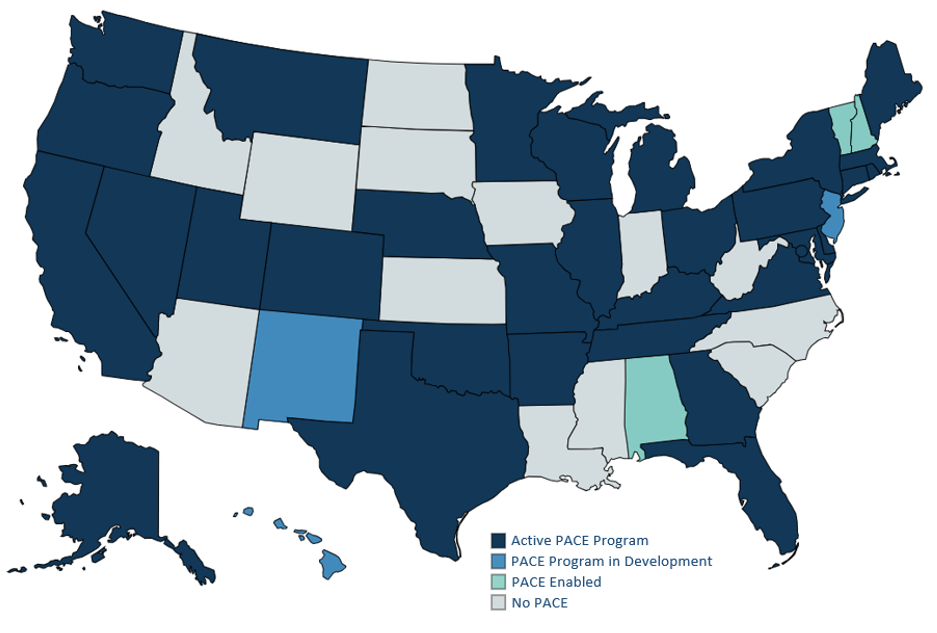

PACE lending programs are controlled or overseen by state and local governments however PACE loans are issued by private capital providers. PACE lending legislation is active in 38 states and Washington DC. Of those states, 30 and Washington DC have active PACE programs that are currently launched and operating [5].

Source: PACENation.org

Economics of C-PACE Financing

C-PACE loans are typically structured with long amortization periods of 20-30 years depending on the useful life of the energy efficient improvements. C-PACE loans are fixed rate and priced with a 300 to 400 basis point spread above a benchmark interest rate which is typically the United States 10-Year Treasury Bill. As of 4Q 2023, this can mean that some C-PACE financing can be less expensive than subordinate financing which typically trades 600 basis points or more above the Secured Overnight Financing Rate (“SOFR”) or other benchmark interest rate.

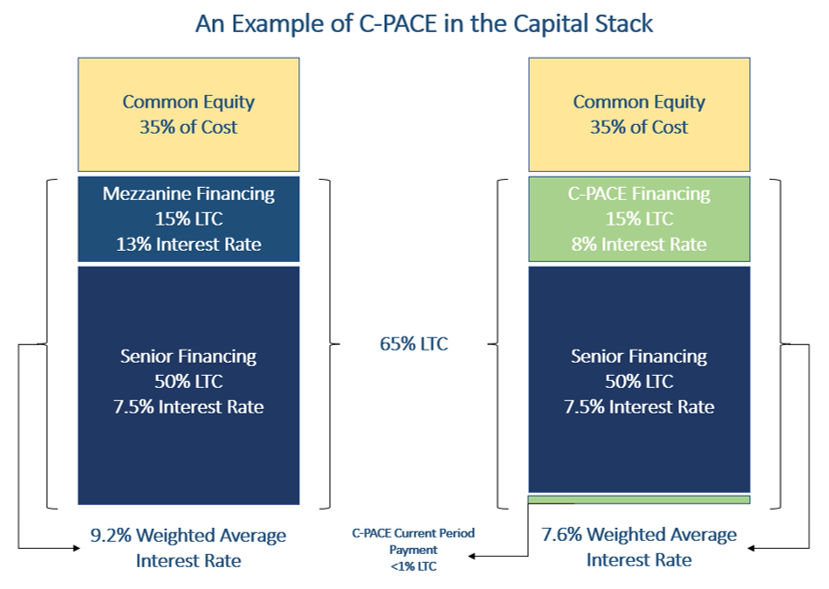

C-PACE loan-to-cost (“LTC”) ratios are determined by the scale of the sustainability improvements being applied to the underlying assets. Before the interest rate tightening cycle, C-PACE loans often comprised of one third to one half of the total debt financing in a project capital stack. As LTC ratios have decreased with the increase in rates and tightening in lending standards, C-PACE loans have financed greater shares of real estate capital structures. C-PACE loans have often been used to completely substitute subordinate financing and in some cases the entire senior mortgage depending on the leverage limitations of the state or local government’s PACE program [6].

When C-PACE financing is used to mitigate the need for mezzanine financing, capital structures may have lower financing costs.

Risks of C-PACE Financing

C-PACE loans being structured as assessments may cause some issues for borrowers looking to sell their asset. Because the financing is structured as an assessment on the property’s tax bill, property level operating expenses will increase, decreasing the net operating income (“NOI”). This is unlike normal financing that does not impact NOI and therefore asset value. The complexity of the structure may cause confusion around property values upon exit as some potential buyers may not be aware of how the C-PACE financing impacts NOI and cap rates.

Additionally, since C-PACE loans cannot be prepaid, they must be assumed by the new buyer upon sale. As a result, securing new financing can be an additional issue for buyers, causing further complications with exiting an asset. Senior lenders may feel uncomfortable with providing financing on a building with a C-PACE loan attached because they are unfamiliar with the structure. In addition, if interest rates were to fall, the property owner would be unable to replace this portion of the capital stack.

Conclusion

C-PACE loans can be a viable option for real estate investors looking to find affordable financing options in a tight lending environment. C-PACE loans can fill gaps in capital stacks that would otherwise need to be financed by expensive subordinate financing.

ORG believes that C-PACE financing is an underexplored area in the real estate investment landscape today. For investors who were otherwise considering making energy efficient improvements on their properties, C-PACE financing can be an optimal solution for decreasing financing costs and adding value all while decreasing long-term utility related expenses. In addition, ORG believes that C-PACE lending could be an interesting opportunity for real estate credit investors to earn high income-oriented returns in the event that interest rates fall.

[1] Laura Rapaport et. al., “C-PACE 101 for Borrowers,” Northbridge

[2] Troy Segal, July 19, 2023, “Property Assessed Clean Energy (PACE) Loan: Overview,” Investopedia, https://www.investopedia.com/terms/p/property-assessed-clean-energy-paceloan.asp#:~:text=A%20Property%20Assessed%20

Clean%20Energy%20%28PACE%29%20loan%20is,energy%20improvements%20at%20a%20commercial%20or%20residential%20property.

[3]“C-PACE for mortgage lenders and mortgage-lender consent,” Nuveen Green Capital, https://www.nuveen.com/greencapital/about-c-pace/c-pace-for-mortgage-lenders.

[4] Laura Rapaport et. al., “C-PACE 101 for Borrowers,” Northbridge

[5] “PACE Programs,” PACENation, https://www.pacenation.org/pace-programs/#!US-MA%202%29%20https://www.pacenation.org/pace-market-data/

[6] September 15, 2023 “Commercial Mortgage Alert – C-PACE Gains Ground on Mortgages,” Green Street