Build-For-Rent Housing: A Solution to Balance Housing Supply

Build-for-rent housing is emerging as a viable solution to the U.S. housing affordability crisis, providing high-quality rental options for families while balancing supply and demand in the residential market.

August 7, 2023

Introduction

Throughout 2022 and 2023, many economists believed that increases in interest rates from the United States Federal Reserve would help to slow the rate of home price appreciation and improve housing affordability. This was because increasing mortgage rates could decrease homebuyers’ appetite at current prices and subsequently keep home prices affordable over the long term. Surprisingly, this slowdown in home price appreciation did not occur because in 1Q 2023, the median sale price of a United States home skyrocketed 32.8% to $436,800 from $329,000 in 1Q 2020. From 1Q 2022 to 1Q 2023, the median home price continued to increase by 0.9% [1].

Despite a muted impact on home price appreciation, the increases in interest rates have had a significant effect on mortgage rates in the United States. In November 2022, the average 30-Year fixed rate mortgage in the United States reached a 20 year high of 7.1% (a 400-basis point increase from the prior year) before moderating to 6.8% in June 2023 [2].

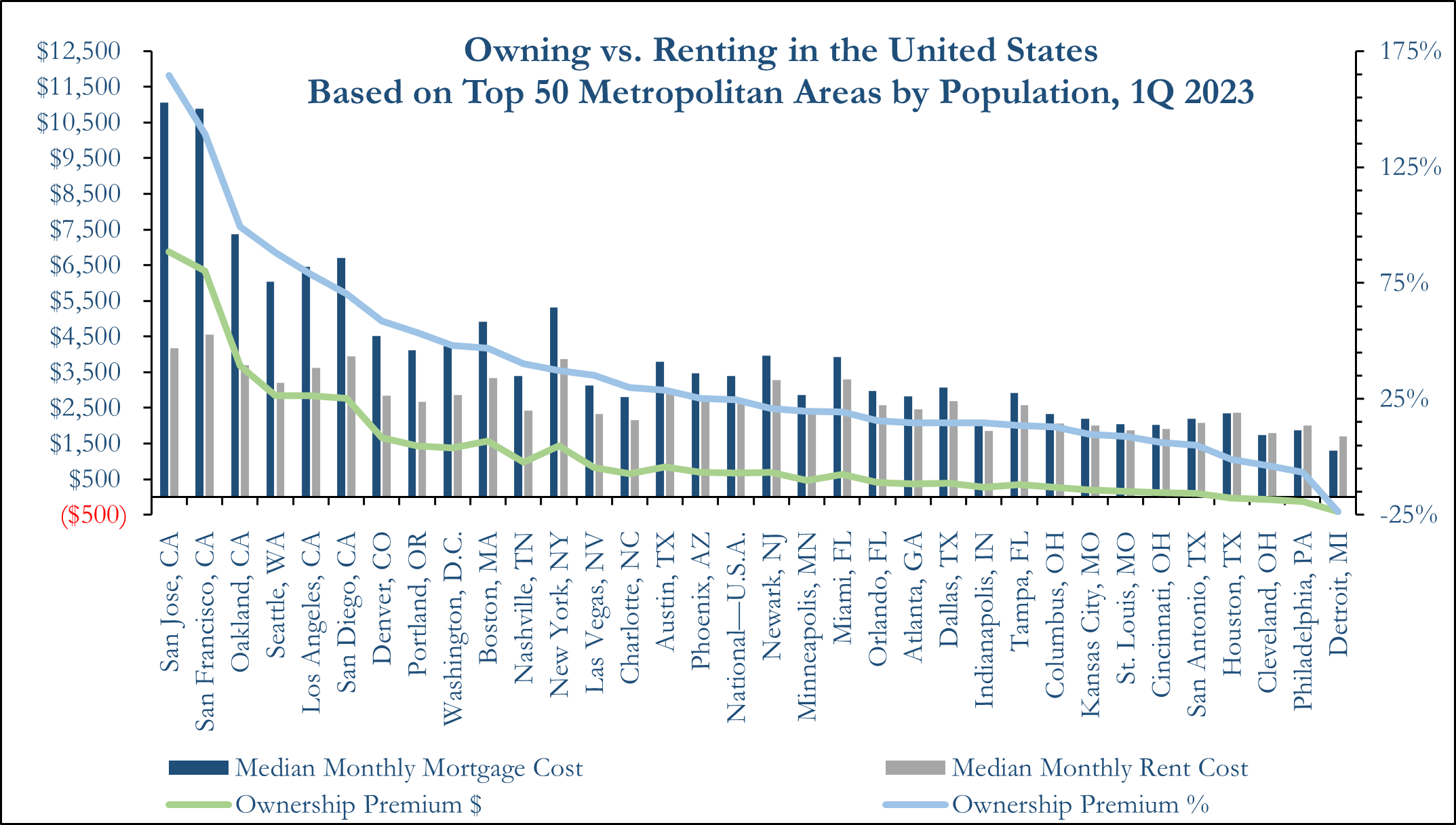

To date, high mortgage rates have substantially increased housing costs. Home prices remaining high combined with the rapid increase in mortgage rates have led to some of the worst housing affordability conditions in United States history. In March 2023, among the top 50 most populated metropolitan areas of the United States there were only four cities, Detroit, Cleveland, Houston and Philadelphia, where it was more affordable to own a home than rent one. The median monthly rental and mortgage payments were $2,715 and $3,385 respectively which equates to a 24.7% or $670 monthly premium to own rather than rent. On average, only 19% of all homes in the top 50 most populated metropolitan areas of the United States were more affordable to own than rent [3].

It is more affordable to rent a home rather than rent a home in 92% of the top 50 most populous metropolitan areas in the United States. Source: Redfin

Increasing the overall supply of housing in the United States should be one the best ways to remedy the housing affordability crisis. ORG believes that Build-For-Rent housing (“BFR”), a subsector of Single-Family Rentals (“SFR”), is a viable strategy for improving overall housing affordability and quality in the United States while allowing investors to optimize their residential real estate portfolios.

Characteristics of Build-For-Rent Housing

BFR housing is a SFR strategy where new homes are constructed specifically for the purpose of leasing as opposed to outright sales. The primary approach to BFR is to construct well-located communities that will serve as housing for the lower and middle-income workforce. BFR communities can be planned as attached townhomes or as detached, stand-alone homes.

BFR housing has some significant advantages in comparison to traditional scattered-site SFR aggregation due to the clustering and uniformity of the units. BFR units can be developed with similar external appearance, structure, internal appliances and fixtures which can be advantageous for property management and maintenance. In addition, BFR housing can attract tenants through community amenities such as parks, pools and neighborhood retail centers.

Young families are the most common living arrangement of BFR tenants because of the appealing amenities, locations and yard space that can provide a great home for them while they save for a down payment. The average household size in SFR properties was 2.9 people per unit while the average for apartments was 1.9 people per unit [4].

BFR communities are also an ideal living arrangement for families who move frequently, are experiencing a transitional period in their lives or are constructing a new home as they can look to BFR housing communities for a shorter-term stay [5]. This way, they can have the comfort of a single-family home with a fraction of the hassle and cost associated with buying and subsequently selling a home. A well located BFR community can also provide lower and middle-income renters with reputable school districts and safe neighborhoods for their children to live and play. Once the time comes to move into a permanent home or move to a different city, the adjustment can be quick and convenient upon expiration of the tenant’s lease. BFR housing is also a favorable solution for younger families who can try living in BFR homes in different areas for as long as they are comfortable before committing to buy a home in a specific neighborhood.

Build-For-Rent as a Solution to Housing Affordability

Many critics have raised issues with the increase in institutional SFR ownership. Their concern is that institutional scattered-site ownership is removing for-sale housing from the market and therefore decreasing the number of homes for purchase. While institutional investment into SFRs remains limited in comparison to “mom-and-pop” SFR investors, the potential for increased institutionalization has led to growing concerns over the supply and demand balance of housing.

BFR communities should not be grouped with scattered-site SFR investments regarding their impact on housing affordability. BFR development nationwide can be a net positive for housing affordability as the increased supply can be additive to the residential market. This will be beneficial for a more balanced homebuying market as BFR communities and homes for purchase can compete once the supply of BFR units is more in line with demand.

BFR communities can also be an affordable long-term solution for lower and middle-income earners to have access to safer and more affordable single-family homes. With today’s homeownership costs, lower and middle-income earners may need to buy a home that is too small or too remote to properly support their family. With an increase in BFR supply, high quality rental units can be accessible to a greater population of renters. These more affordable and better located BFR units will allow lower income earners to establish their families in safe neighborhoods and better school districts.

Build-For-Rent Market Fundamentals

Institutional investors today have an increased interest in BFR to capitalize on the demographics of renters outlined above. This is reflected by the increase in market share of rental housing construction starts as a percentage of total housing construction starts. In 2022, 6.9% of all home construction starts were single family rentals which is a 32.7% increase from 2021. The total amount of BFR starts in 2022 was over 69,000 [6].

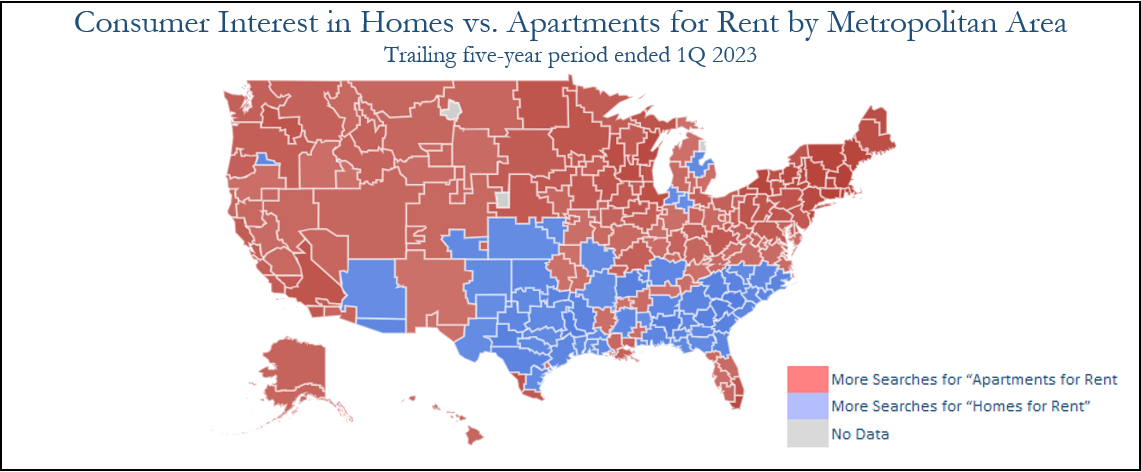

ORG believes that BFR housing investments will perform best in areas of the Sunbelt United States with high job growth and high rates of family formation. These markets are the most viable for investment as they have a large spread between home rental costs and home ownership costs while also being favorable for residential real estate investors in regard to taxation and regulation. In addition, most Sunbelt markets have seen more demand in homes for rent as opposed to traditional multifamily apartment rentals. Over the five-year period ending 1Q 2023, Google Search data shows that multiple Sunbelt states including Georgia, North Carolina, South Carolina and Texas had more interest in the search term “Homes for Rent” than “Apartments for Rent”. Many submarkets across the Sunbelt and some outliers such as Bend, Oregon and Saginaw, Michigan exhibited the same trend.

Most areas in the Sunbelt exhibited more interest in Homes for Rent rather than Apartments. Source: Google Trends

Build-For-Rent Investment Environment

BFR and SFRs as a whole experienced strong fundamentals during the first quarter of 2023. Occupancy rates for SFRs were 94.4% in 1Q 2023 which is a slight decrease from their recent highs of 95.3% in 2Q 2021.

The average valuation for investor-owned SFRs was $354,000 per unit in 1Q 2023 which is a 12% discount to the average price of an owner-occupied single-family home. Cap rates for SFRs in 1Q 2023 were 5.9% on average which is their highest level since 3Q 2020. SFRs on average traded at an 84-basis point cap rate spread above traditional multifamily property investments and a 227-basis point spread above the 10-Year treasury reflecting an attractive risk premium for the sector [7]. In the BFR sector today, investors can reasonably expect to achieve development yields greater than 6% [8]. BFR investors may also be able to secure more favorable financing due to increased access to agency lending.

Today, ORG believes that BFR investing will be beneficial for investors of all sizes. BFR investments will allow for smaller investors to own and operate an SFR portfolio with adequate operational efficiency without the vast personnel and technology requirements for a scattered-site investment approach [9] much like a traditional multifamily property. They also will not need to compete with large scattered-site aggregators with significant economies of scale who have advanced acquisition algorithms and balance sheet flexibility to have in house software engineering and data science departments. Large investors can also adequately compete in the market as they can develop, operate and acquire BFR properties much like they could in any other multifamily property portfolio.

Conclusion

BFR communities are a residential real estate sector with unique competitive advantages. BFR housing can appeal to a variety of different renters for which traditional multifamily units may not be ideal. From families who are frequent movers, lower and middle-income renters or potential homebuyers, BFR has a wide range of potential tenants.

Sunbelt markets of the United States present the best conditions for BFR investment due to their attractive renter demographic and real estate investor-friendly taxes and regulations. Investors of all sizes will be able to properly compete in the BFR space due to the operational similarities to traditional multifamily.

BFR housing development should be one of the most viable ways to help combat the housing affordability crisis in the United States today. With an average 24.7% monthly premium to own a home today [10], many potential homebuyers are priced out of the market. An increase of BFR housing supply may help to provide fair access to safe neighborhoods and strong schools for all Americans.

[1] 2023, “Median Sales Price of Houses Sold for the United States,” Federal Reserve Economic Data, https://fred.stlouisfed.org/series/MSPUS.

[2] 2023, “30-Year Fixed Rate Mortgage Average in the United States,” Federal Reserve Economic Data, https://fred.stlouisfed.org/series/MORTGAGE30US/.

[3] Lily Katz & Taylor Marr, May 19, 2023, “There Are Only Four Major U.S. Metro Areas Where It’s Cheaper to Buy a Home Than Rent,” Redfin News, https://www.redfin.com/news/rent-vs-own-2023/.

[4] Claire Gray, September 28, 2021, “An Overview of Single-Family Rentals,” NMHC, https://www.nmhc.org/research-insight/research-notes/2021/an-overview-of-single-family-rentals/.

[5] January 16, 2020, “The New Face of Rental Housing: Single-Family Built-For-Rent,” Forbes, https://www.forbes.com/sites/bradhunter/2020/01/16/the-new-face-of-rental-housing--single-family-built-for-rent/?sh=35e69a083a10.

[6] 2023, “Single-Family Rental Investment Trends Report Q1 2023,” Arbor, https://arbor.com/research/single-family-rental-investment-trends-report-q1-2023/.

[7] 2023, “Single-Family Rental Investment Trends Report Q1 2023,” Arbor, https://arbor.com/research/single-family-rental-investment-trends-report-q1-2023/.

[8] John Pawlowski et. al., April 20, 2023, “Conference Insights: SFR: Discerning Through the Dichotomy,” Green Street

[9] John Pawlowski et. al., April 20, 2023, “Conference Insights: SFR: Discerning Through the Dichotomy,” Green Street

[10] Lily Katz & Taylor Marr, May 19, 2023, “There Are Only Four Major U.S. Metro Areas Where It’s Cheaper to Buy a Home Than Rent,” Redfin News, https://www.redfin.com/news/rent-vs-own-2023/.