January 31, 2024

2024 United States Real Estate Market Outlook

Introduction

2023 was a year that surprised many investors as the potential economic recession that was seemingly imminent at the beginning of the year never materialized in a meaningful way. Economic conditions were favorable for many investment sectors with falling inflation, steady corporate earnings, low unemployment and high economic growth all being capped off by the United States Federal Reserve hinting at multiple interest rate decreases in 2024.

For real estate investors, the year was not quite as positive with investment volume remaining at record lows and wide bid-ask spreads bringing current real estate valuations into question. In this article, ORG will provide a review of the real estate markets in 2023 and what investors should look forward to in 2024.

2023 In Retrospect

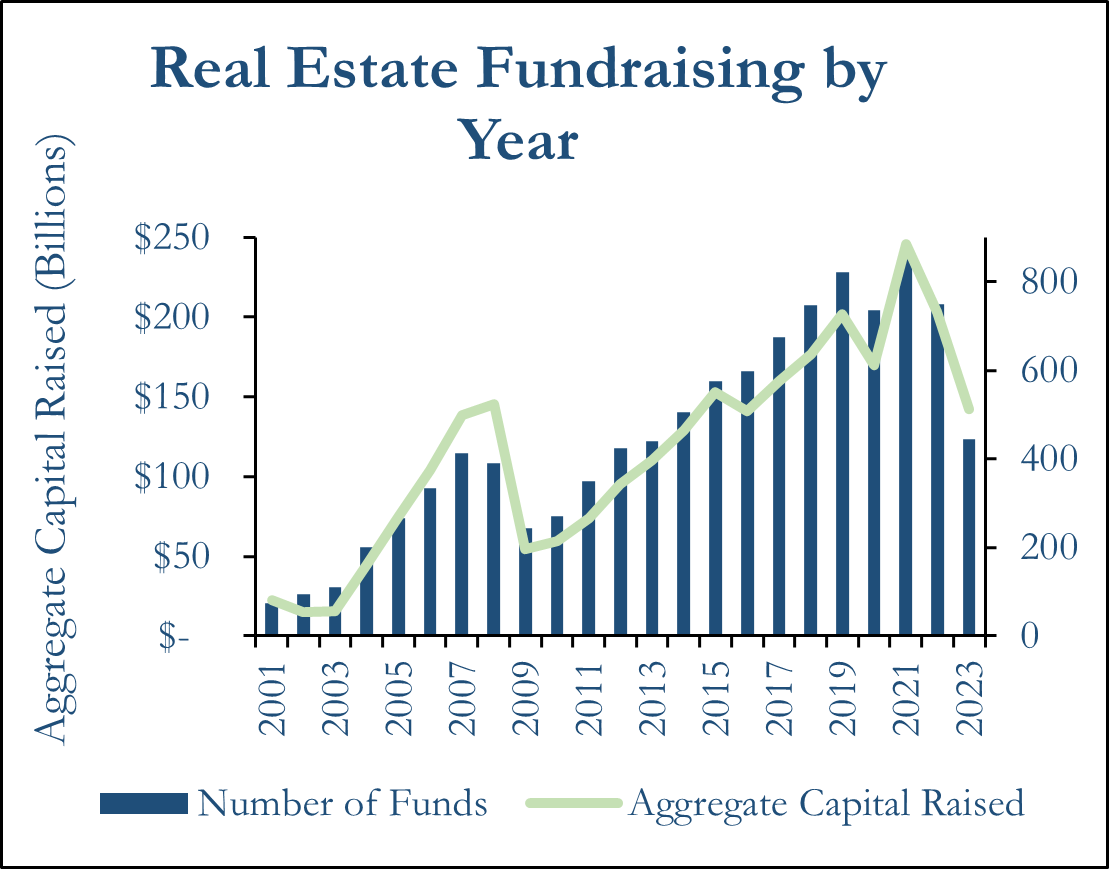

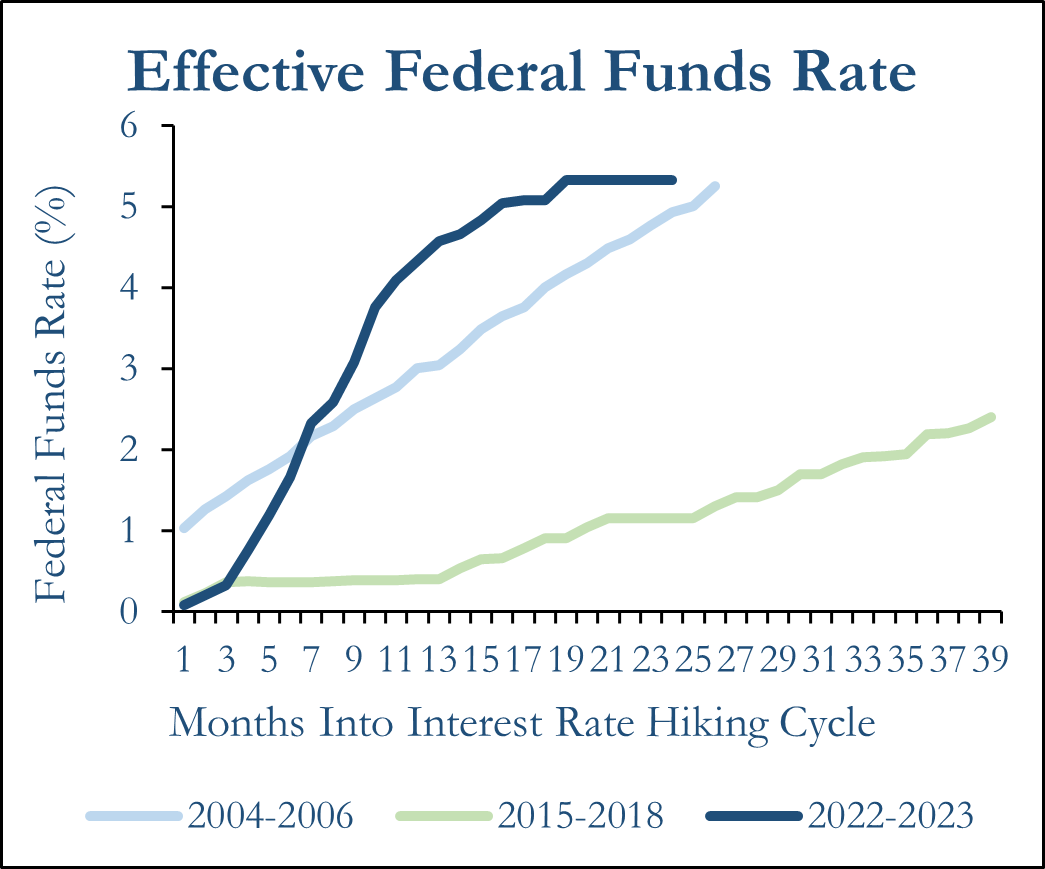

Amid uncertainty of peak interest rates, inflation expectations, work-from-home, housing affordability and questions of the continued strength in industrial, many investors remained on the sidelines with low levels of fundraising and capital deployment. As a result of low market liquidity, ORG expected capital structure dislocation to remain a consistent theme and that pivoting into real estate credit strategies would be a favorable investment approach. Real estate credit proved to be a viable strategy throughout the year as liquidity became increasingly scarce. The regional banking crisis in March 2023 that caused the downfall of Silicon Valley Bank and First Republic Bank essentially eliminated regional banks from being reliable sources of financing for real estate sponsors. This coupled with the increases in base rates and spreads gave rise to opportunities to earn double-digit returns in real estate credit without taking equity risk.

Real Estate fundraising hit its lowest level since 2016. Source: Preqin

The Federal Funds Rate reached 5.25%-5.50% in July 2023. Source: FRED

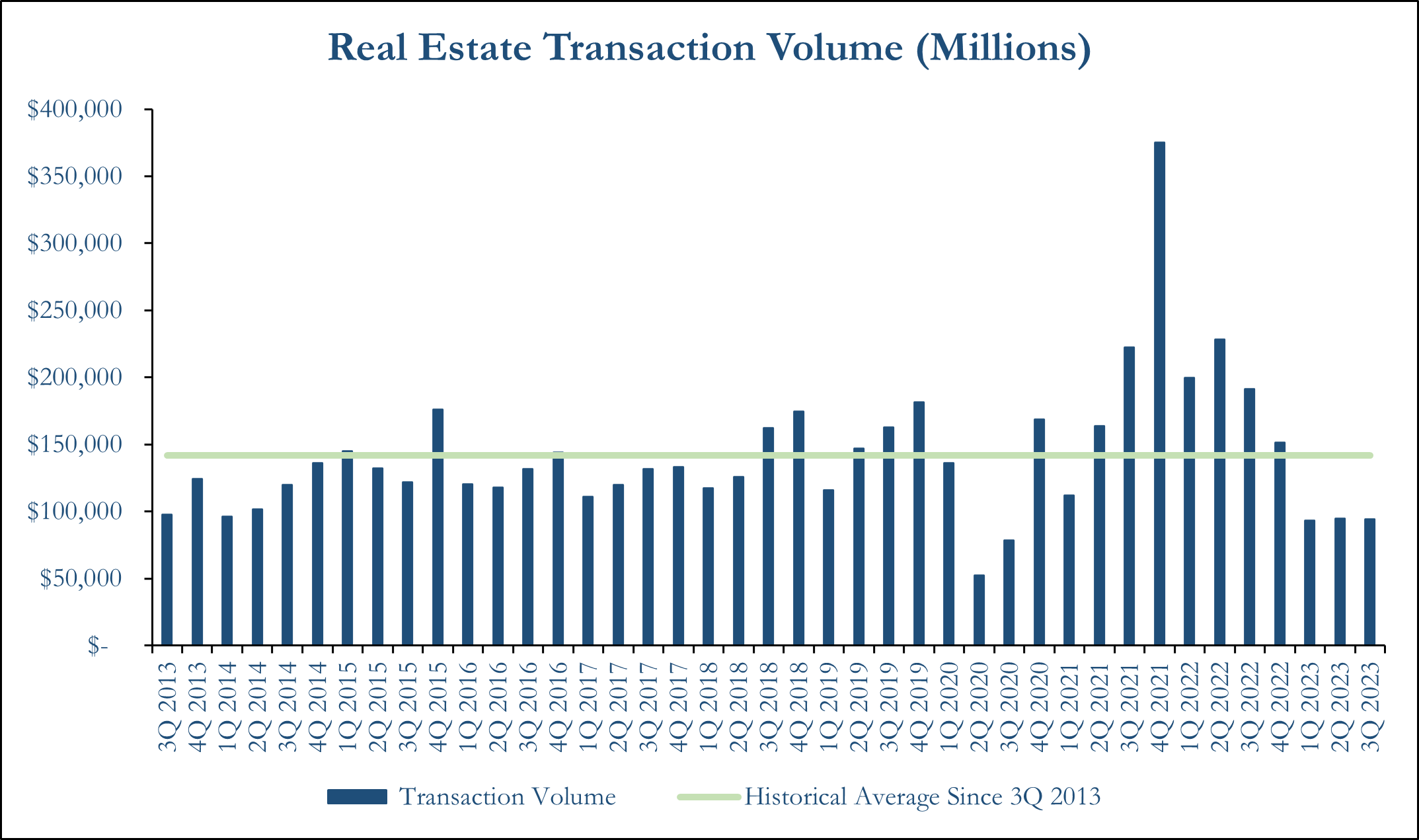

Heading into 2023, ORG expected redemption queues in open-ended core funds to cause large scale distressed selling to pay down said redemptions. This did not materialize as a significant theme since returns in other asset classes, namely public equity holdings, helped to ease the denominator effect issues of many institutional investors which prompted the redemption requests. The easing of redemption queues also had the tangential effect of reducing the volume of attractive secondary purchases of limited partner fund interests. Core buyers also remained on the sidelines further contributing to the extremely low real estate transaction volumes during 2023. Nonetheless, redemption queues are still high and remain at approximately 10% to 20% of net asset value for most open-ended core funds compared with approximately 0% to 5% before the COVID-19 Pandemic (4Q 2019). As a result, we believe that the liquidity of these funds should be closely monitored throughout the coming months.

Real Estate Transaction Volume has been low in comparison to recent years throughout 2023 as institutional capital deployment and core fund investment activity remains low. Source: Real Capital Analytics

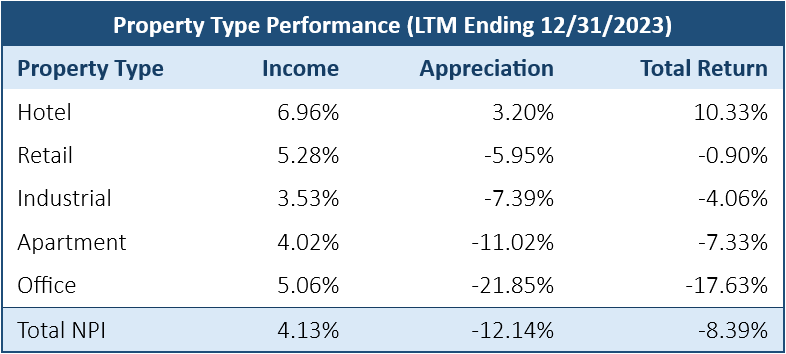

Core real estate returns were largely disappointing as cap rate expansion and slowing growth weighed on asset values, however the market did not experience the significant downturn that many expected. Over the past 12 months, the best performing property types in the NCREIF Property Index (“NPI”) have included hotels, retail and industrial. Apartment returns were disappointing and significant weakness in the office sector persisted. All of the major property types saw negative performance during the year ended 4Q 2023 aside from hotels.

Source: NCREIF Property Index

Retail surprised many with its outperformance which was mainly a result of more conservative market pricing and steady demand for service-based retail, necessity neighborhood strip centers and grocery anchored centers. Industrial posted negative returns, largely because of slight cooling in leasing demand and occupancy decreasing by 41 basis points in the twelve months ended 4Q 2023. Additionally, industrial cap rates continued to normalize from their extremely compressed levels in 2021 and 2022, increasing from 3.56% to 4.09% in the twelve months ended 4Q 2023 [1]. Apartments also weakened as rent growth continued to slow. Quarter-over-quarter apartment rent growth was -0.75% and -0.59% on average in the United States in 3Q 2023 and 4Q 2023 respectively. Over the twelve months ended 4Q 2023, apartment rent growth slowed to 0.69% from 3.7% a year earlier [2]. Financing costs for new loans became a risk for recently developed apartments and existing apartment assets with loans maturing.

Office continued to disappoint in 2023 as significant declines in demand for space and essentially non-existent capital markets for the sector simultaneously decreased performance. Suburban office slightly outperformed central-business district (“CBD”) properties however both CBD and suburban office performance across all geographies of the United States underperformed the unlevered total NPI [3].

Outlook for 2024

ORG believes the current environment sets up well for dynamic and prudent investors to achieve significant outperformance. Despite this, some strong investment strategies may soon see their window of opportunity close in the coming months.

Real Estate Credit

Real estate credit continues to be the preeminent theme in the asset class today. With the significant rise in interest rates since 2022 and the nearly $2.2 trillion in commercial real estate debt maturities through 2027 [4], upcoming refinancings will be a theme that should be closely monitored.

2023 was an attractive year for real estate credit opportunities. Senior financing positions could see rates up to 9% for some assets while subordinate debt investments could achieve all in rates in the mid-teens. However, in the current environment and looking forward to year end, ORG believes that the availability of these opportunities will be increasingly fleeting. This is because of the Federal Reserve’s indication toward preventing real interest rates from becoming overly restrictive to future economic growth as inflation decreases. Our expectation is that barring significant tightening in labor market conditions, the Federal Funds Rate may decrease by 50 to 75 basis points by the end of the year with the longer run Federal Funds Rate settling around 2.5%-3.0%.

Real estate credit funds have been an attractive investment opportunity because of the capital markets dislocation since the United States Federal Reserve began to increase interest rates in March 2022. Now with the anticipation of interest rate cuts, we do not believe that the opportunity to invest in closed-ended opportunistic credit funds will be quite as interesting. ORG believes that the environment for lending opportunities could become increasingly competitive which could drive down long-term returns in credit funds with investment periods of two to three years. Because of this, ORG believes that opportunistic real estate funds that have the flexibility to invest across the capital stack in both credit and equity are more favorable than pure-play credit funds. Additionally, individual investments in structured real estate credit could still prove to be attractive since investors can be more intentional about what assets, borrowers and returns they are seeking with more precise timing than a closed-end credit fund.

Investment Structures

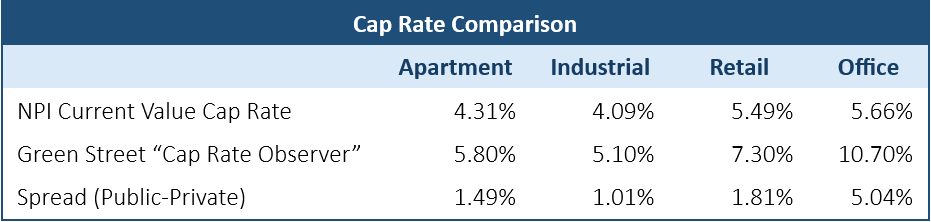

In 2024 we believe that the prudent and active real estate investors will be able to find strong outperformance in non-core real estate funds with capital stack flexibility and skilled investment managers as opposed to traditional core open-ended real estate equity funds. Despite having some decline in values throughout 2023, we still believe that open-ended core funds may have double-digits of additional markdowns to come throughout 2024. Many assets held within open-ended core funds, while high quality, seem to be overvalued on a cap rate basis relative to their peers in the public markets. Low transaction volumes over the past year also seem to support the case that the “market clearing price” for real estate assets held within open-ended core funds has yet to be found.

A large spread between public and private cap rates remains in the market. Sources: NCREIF, Green Street Cap Rate Observer December 2023

ORG also believes that direct investments and co-investments in real estate across the capital stack will be attractive. The dislocation in capital markets today presents a unique opportunity for institutional investors to partner with skilled managers in need of co-investment capital to achieve outsized returns with a more favorable fee load.

Property Types

All real estate property types face capital markets headwinds going into 2024. Despite this, fundamentals remain generally strong despite higher cap rates and discount rates.

Industrial has remained the most desirable sector for investors with both equity capital and debt financing more readily available than any other property type. Long-term fundamentals, for logistics properties in particular, remain strong as tenant earnings and balance sheets remain robust. Economic tailwinds such as supply chain onshoring and e-commerce growth continue to be prevalent which is additive to the value and scarcity of well-located infill logistics properties. In the near term, however, some continued negative performance is to be expected with expanding cap rates, increasing vacancy and slowing rent growth in the sector.

Retail continues to remain a sector of cautiously high conviction for ORG. A combination of a reasonable cap rate environment and availability of positive leverage makes core and value add acquisitions a viable strategy in today’s environment. Many of the remaining retail tenants that currently have strong credit have “survived” the rise of e-commerce and are likely to continue drawing high demand from consumers. We expect service based, grocery-anchored and neighborhood retail centers to continue their strong performance into 2024.

We expect multifamily to face headwinds in 2024, however the long-term fundamental housing shortage in the United States will allow the broad sector to remain somewhat resilient. Many markets in the United States are facing slowing rent growth as a result of new supply and a slowdown of in-migration to the Sunbelt markets that became popular during the COVID-19 pandemic. Many recently developed assets will likely be in need of subordinate debt to fill the gap that has been created from increasing financing costs and higher debt service coverage requirements. As a result, ORG believes that the most ideal way to invest in the multifamily sector will be through targeted subordinate debt opportunities that are able to fill the gap in multifamily capital structures. In regard to quality, we believe that workforce housing that appeals to tenants who earn 80%-120% of Area Median Income will be the most attractive to own and develop.

Office remains a sector with poor fundamentals and nonexistent capital markets. We believe that working remotely will be a mainstay in all markets as return-to-office data has remained lackluster even in favorable Sunbelt growth markets. We expect pricing to eventually correct to a level that is comfortable for investors to reposition obsolete office assets, however we do not expect this to occur in 2024.

We believe that the more desirable office strategy is in the medical office sector, as an aging demographic in the United States and overall increased emphasis on healthcare in the post-pandemic era will lead to vastly stronger absorption and tenant credit. Because of these demand drivers, ORG still holds high conviction in the portfolio aggregation strategy of medical office properties. We believe that investors may be able to achieve cap rate compression in the sale of medical office portfolios to large, core capital allocators.

The data center sector had a surprising emergence during 2023 with extremely strong returns and robust tenant demand catching the attention of many investors. In the public markets, the data center REITs Digital Realty (NYSE: DLR) and Equinix (NASDAQ: EQIX) saw share price increases of 31% and 22% respectively in 2023. The growth of artificial intelligence excitement and continued technological innovation worldwide gave rise the best data center leasing year in 2023 (approximately 4500 total megawatts) with three consecutive quarterly leasing records in 2Q, 3Q and 4Q 2023[5]. The positive fundamentals in the sector have piqued our interest and we believe that development strategies with high barriers to entry and development yields in the 8%-11% range will be attractive for investment.

Conclusion

ORG believes that 2024 will be a strong year for dynamic investors to invest into private real estate opportunities. Although core real estate assets seem to be overvalued, opportunistic and value add opportunities are beginning to become more attractive as cap rates expand and leverage becomes more accretive to returns. We believe that the most attractive investment opportunities in 2024 will be with managers who can effectively invest across the entire capital stack, as well as preferred equity and special situation equity co-investments.

[1] “NCREIF Property Index – 4Q 2023 Trends Report” NCREIF.

[2] “CoStar Data Export – United States Multifamily” CoStar.

[3] January 25, 2024 “NCREIF Property Index – Quarterly Detail Report” NCREIF.

[4] Peter Grant, January 16, 2024 “The Bill Is Coming Due on a Record Amount of Commercial Real Estate Debt” The Wall Street Journal.

[5] David Guarino, January 19, 2024 “Data Center: 4Q23 Industry Data – Wanted: Synonym for ‘Record’” Green Street.