June 1, 2023

Medical Office Buildings:

The Crown Jewel of Office Real Estate

Introduction

In the wake of the COVID-19 pandemic Medical Office Buildings (“MOB”) had solid performance, unlike traditional office. This is primarily due to MOBs being unaffected by work-from-home because of medical procedures requiring in-person attention and specialized equipment to be performed properly. Patients were also resistant to telemedicine with nearly two thirds of Americans preferring to visit their doctor in person [1].

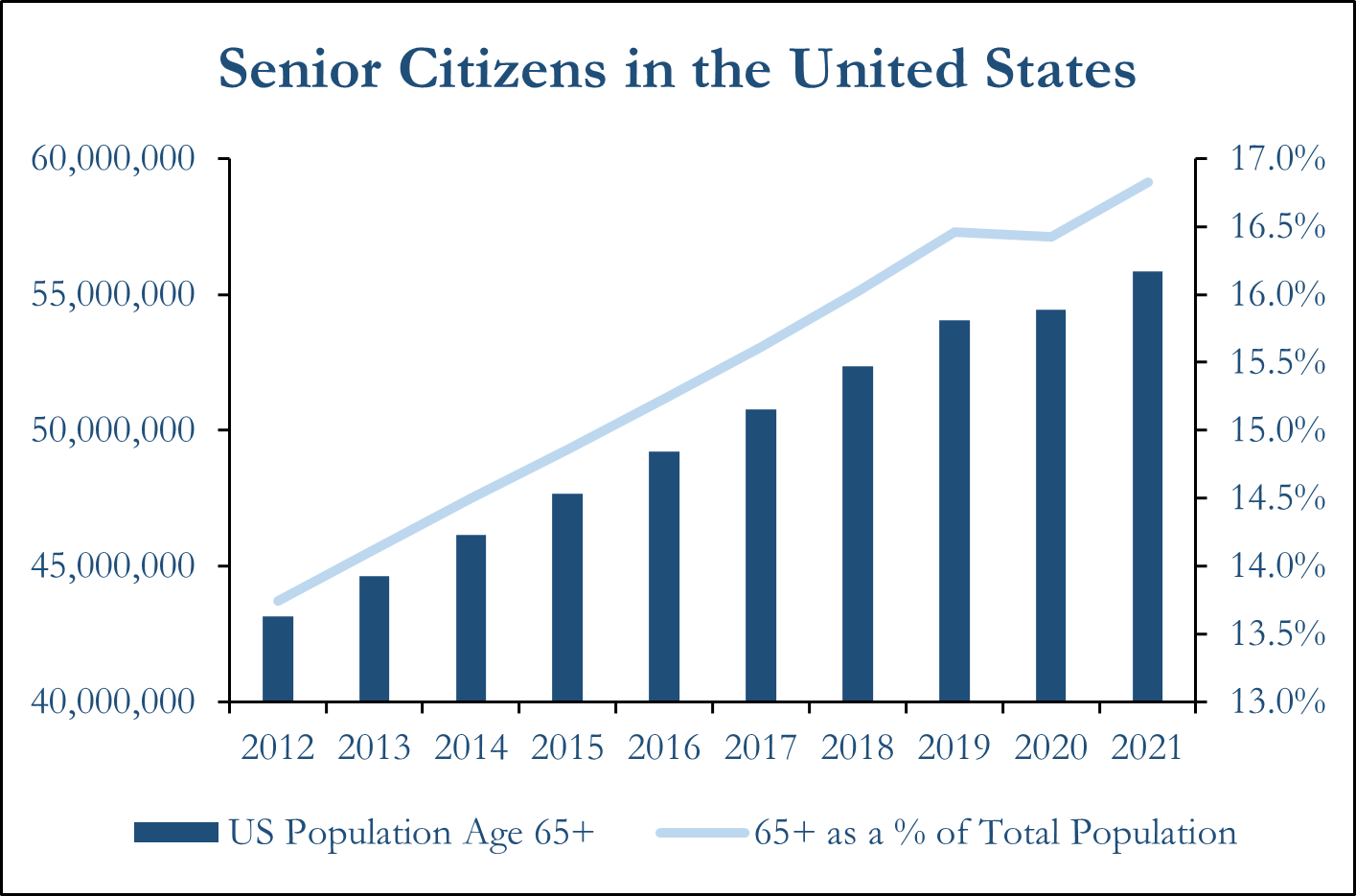

The aging population of the United States is another tailwind for MOBs. As of year-end 2021, 16.83% of the United States population was over 65 years of age [2]. This is significant because in the United States, people aged 65+ will make on average 4.98 doctor’s visits per year. In comparison, Americans aged 18-44 and 45-64 make on average 1.90 and 3.02 annual medical visits respectively [3].

The population of 65+ individuals in the United States increased by 29.48% from 2012-2021 while the total population of the United States increased by only 5.74%. Sources: USAFacts.org, US Census

In this article, ORG will discuss the characteristics of MOBs and what investment strategies are viable in today’s environment.

What are Medical Office Buildings?

MOBs are properties that are leased to various medical practices. Some common medical tenants include primary care, pediatric care and specialty medical tenants such as imaging centers, surgery centers, cancer treatment centers, dialysis centers, medical laboratories, dentists and orthodontists.

MOB locations are either categorized as on-campus or off-campus depending on their distance from a nearby hospital or healthcare campus. On-campus MOBs are located within the hospital system or healthcare campus while off-campus MOBs are instead located closer to their patients. In some cases, off-campus MOBs may be associated with a larger hospital system despite being located outside of a major metropolitan area or healthcare campus [4].

An on-campus MOB (Left) versus an off-campus MOB (Right). Suburban off-campus MOBs could outperform due to lower competition and proximity to patient population. Sources: Milwaukee Regional Medical Campus, Cooper Carry

Leasing & Tenancy

MOB leases can be structured as gross or net but are typically structured as triple net (“NNN”). Today, MOB rents average around $24 per square foot per year NNN but can vary depending on the market, tenant and building size [5].

Tenant credit can vary depending on the size of the medical practices with larger medical corporations having stronger credit than small firms. Tenant credit can be enhanced when the MOB tenant is associated with a large regional medical system. Lease guaranties may provide additional protection for MOB leases through associated hospital systems which adds security and value to the MOB lease. Leases may be personally guaranteed by owners of smaller medical practices with no affiliation to a larger hospital system [6].

MOB tenants are likely to renew their leases upon expiration and often have long tenures in one space. MOB tenancy tends to be sticky once the MOB tenants establish their practice within a building. A reason for this is due to the complicated setup process for MOB tenants to personalize their space. With costly build outs and expensive equipment, it is far more economically feasible for MOB tenants to stay in their space over long periods. TI allowances for MOB tenants can range from $100-$120 per square foot. Due to the expensive TIs, MOB owners are compensated with longer lease terms which often last 7-10 years [7].

In addition, medical practices prefer not to move office locations often because their patients may find relocations to be confusing or frustrating. To build a rapport with their patients, it is important that medical practices have a consistent location. Finally, due to the necessity of medical professionals to work in person, there is less risk of obsolescence and less of a need for special amenities to attract workers to the office unlike traditional office buildings today.

As a result of the high quality of MOB tenants and favorable terms of their leases, the sector is becoming a desirable area for institutional real estate investment.

Investment Strategy

In today’s investment environment it is important to have a clear understanding of the risks and opportunities associated with specific markets and investment strategies.

Market Selection

The highest performing MOBs have historically been high barrier to entry, gateway markets with large patient populations. These markets, which include South Florida, New England, Southern California, and the Pacific Northwest [8], have achieved the highest occupancy and rental growth among all markets in the United States [9].

ORG believes that this strategy is not the most optimal in today’s environment. Secondary and tertiary markets have been a beneficiary of out-migration due to COVID-19 and remote work. Dominant medical practices will perform well in these markets as they continue to grow and have lower competition than larger medical practices in highly populated metropolitan areas. Because of this, ORG finds small to mid-sized off-campus MOBs in secondary and tertiary markets throughout the Midwest and Southern United States to be the most attractive for investment today.

Investment Strategy & Exit

An aggregation strategy of dominant medical practices in smaller markets is more favorable than targeting large, core assets in gateway markets. In many cases small to mid-sized MOBs are available for purchase due to the senior partners of owner-user medical practices within MOBs seeking to exit ownership of the real estate. Often, they will execute a sale-leaseback agreement to unlock the equity value of their real estate. Private equity firms who invest in medical practices prefer that the MOBs are owned by third parties to keep balance sheet assets light and keep management focused on operations.

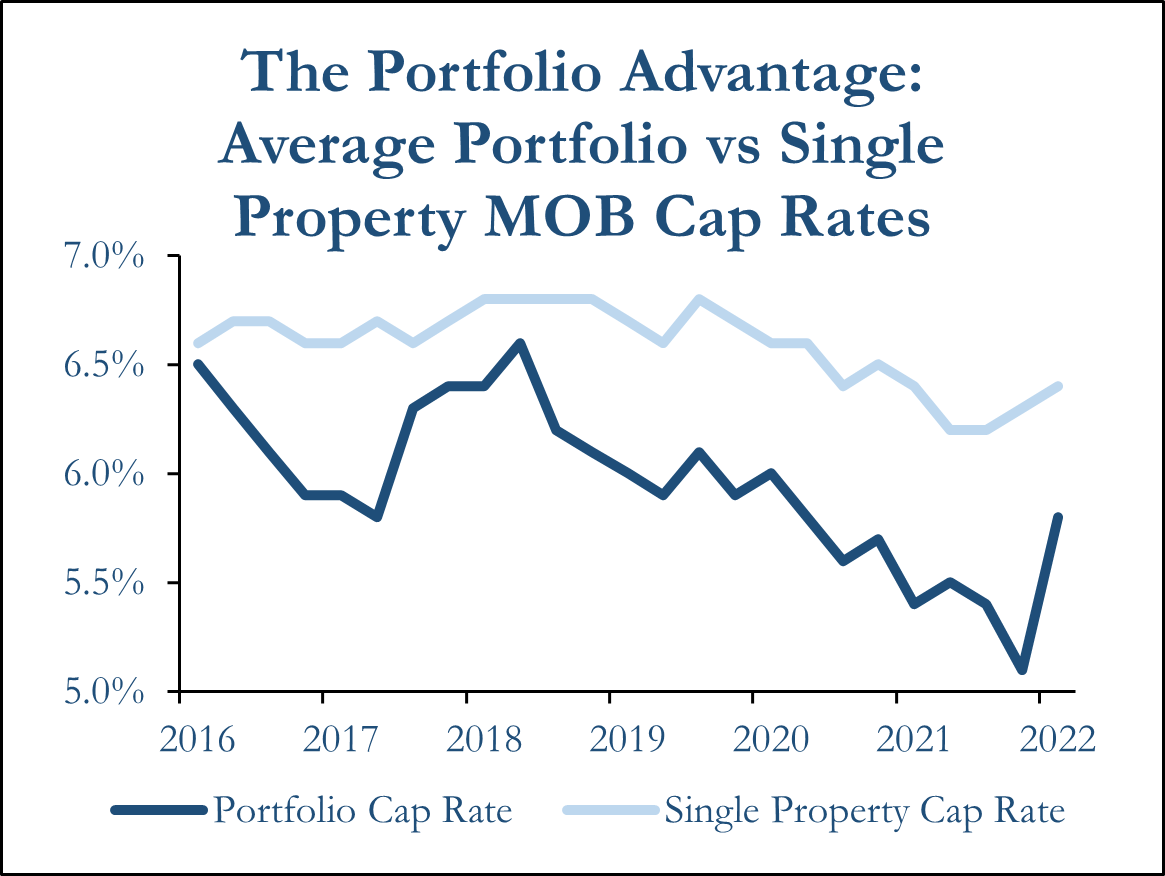

ORG believes a portfolio aggregation strategy of these opportunities will give investors a significant advantage as sales of aggregated portfolios have become increasingly popular and attractive to large institutional buyers. Portfolio sales are preferable to single asset sales for institutional investors and will command considerable cap rate compression for sellers. In 4Q 2022, the average cap rate spread for portfolio sales was 60 basis points lower than single property sales [10].

Portfolio sales trade at compressed cap rates in comparison to individual property sales. Sources: Colliers, Revista

Conclusion

MOBs are a unique and attractive real estate sector with a compelling upside. They have proven to be more resilient than traditional office buildings during the pandemic due to their insulation from the remote work trend. Age demographics in the United States also favor the sector as the aging population increases demand for medical services.

MOBs have a diversified pool of tenants and their tenancy is sticky due to the difficulties related to moving locations. Their expensive and specialized buildouts and their desire to retain long-term relationships with patients also cause them to be resistant to moving. MOBs perform well in secondary and tertiary markets where their tenants are the dominant practice. By aggregating a group of MOBs and exiting through a portfolio sale, investors may expect a premium as opposed to sales of individual buildings.

In today’s market, MOBs are an appealing opportunity for investors to diversify their office portfolio to be better insulated from work-from-home risk and allow them to capitalize on shifting age demographics in the United States.

[1] October 2021, “Household Experiences in America During the Delta Variant Outbreak,” NPR, https://media.npr.org/assets/img/2021/10/08/national-report-101221-final.pdf.

[2] July 2022, “Our Changing Population: United States,” USA Facts, https://usafacts.org/data/topics/people-society/population-and-demographics/our-changing-population?utm_source=bing&utm_medium=cpc&utm_campaign=ND-DemPop&msclkid=20ebfc59ac8517c986c0987a9434361a.

[3] January 2019, “Characteristics of Office-based Physician Visits, 2016,” CDC, https://www.cdc.gov/nchs/products/databriefs/db331.htm

[4] 2023, “Healthcare Investor Survey and Trends Outlook,” JLL, https://www.us.jll.com/content/dam/jll-com/documents/pdf/research/emea/uk/jll-healthcare-investor-survey-and-trends-outlook.pdf.

[5] Shawn Janus et al., March 24, 2023, “2023 Healthcare Marketplace,” Colliers, https://www.colliers.com/en/research/healthcare-marketplace-2023.

[6] June 7, 2022, “Lease Guaranties + Lease Trends in Healthcare,” https://www.matthews.com/thought-leadership-lease-guaranties-lease-trends-in-healthcare/.

[7] Coy Davidson., July 8, 2022, “The Nuances of Leasing Medical Office Space,” Colliers, https://www.coydavidson.com/healthcare/leasing-medical-office-space/.

[8] July 2021, “An Aging Nation, Median Age by County: July 1, 2021,” United States Census, https://www.census.gov/content/dam/Census/library/visualizations/2022/comm/county-median-age.pdf.

[9] Maddie Holmes et al., 2022, “2022 Healthcare and Medical Office Perspective,” JLL https://www.us.jll.com/content/dam/jll-com/documents/pdf/research/jll-us-2022-healthcare-and-medical-office-perspective.pdf.

[10] Shawn Janus et al., March 2023, “2023 Healthcare Marketplace,” Colliers, https://www.colliers.com/en/research/healthcare-marketplace-2023.