Multifamily Preferred Equity - A Point-in-Time Opportunity

Amid rising interest rates and capital market dislocation, multifamily preferred equity presents a unique opportunity for investors to achieve equity-like returns on debt-like investments by filling gaps in stressed capital structures.

March 29, 2024

Introduction

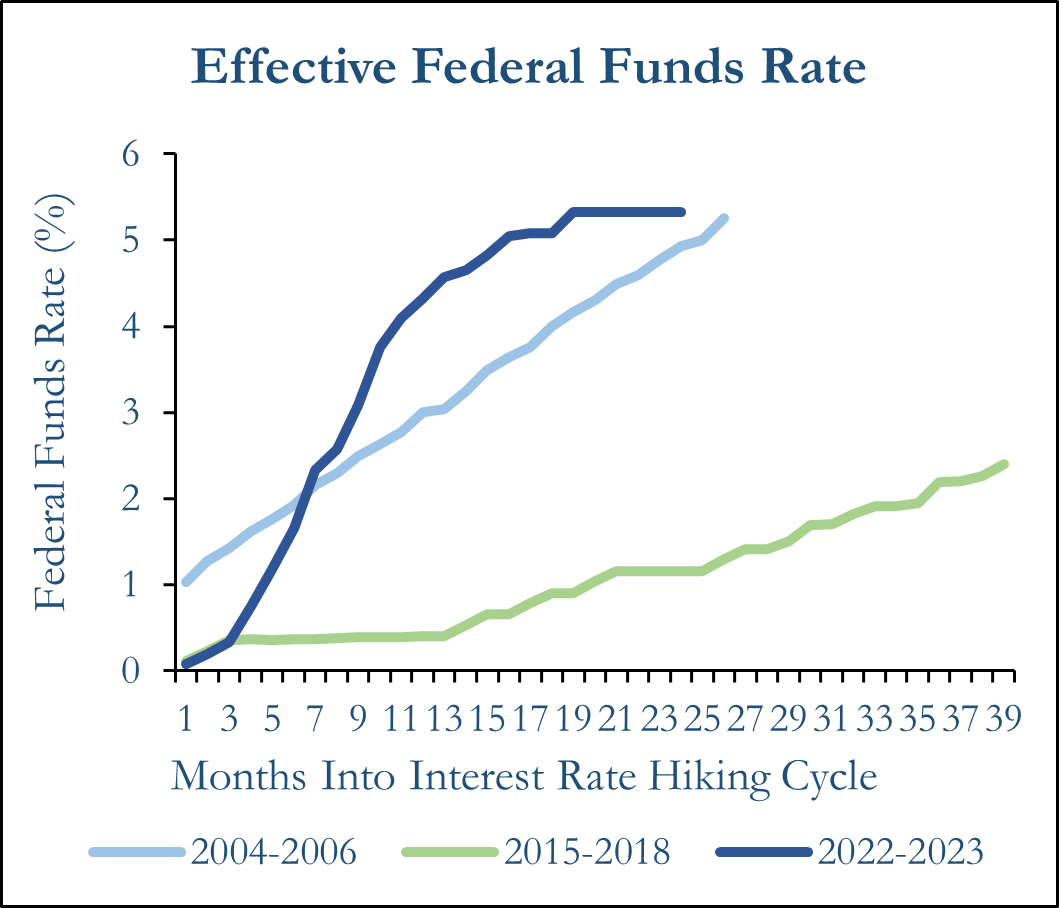

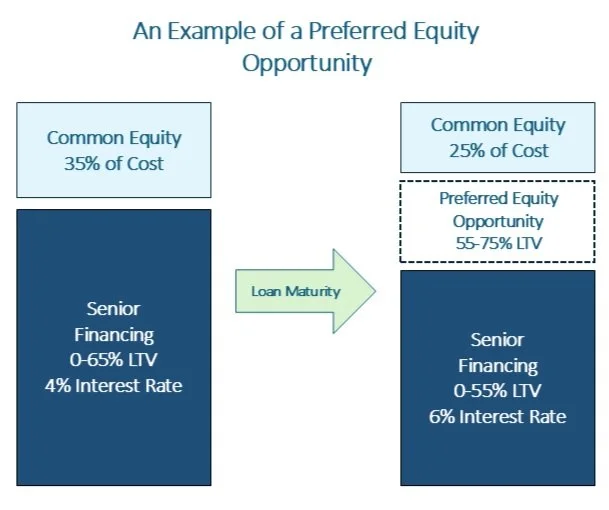

Since the United States Federal Reserve began increasing interest rates in March 2022, the Federal Funds rate increased from a target range of 0.00%-0.25% to 5.25%-5.50% today. This has been a significant catalyst for dislocation in the real estate investment landscape. Many lenders, namely commercial banks under intense scrutiny by governmental regulating bodies, have tightened their lending standards and limited real estate lending. In conjunction with the low availability of financing, borrowers with upcoming loan maturities may be forced to refinance at higher interest rates and lower loan-to-value (“LTV”) ratios. As a result, a gap in the capital structure from approximately 55%-75% LTV may arise which could leave borrowers in need of an alternative financing solution.

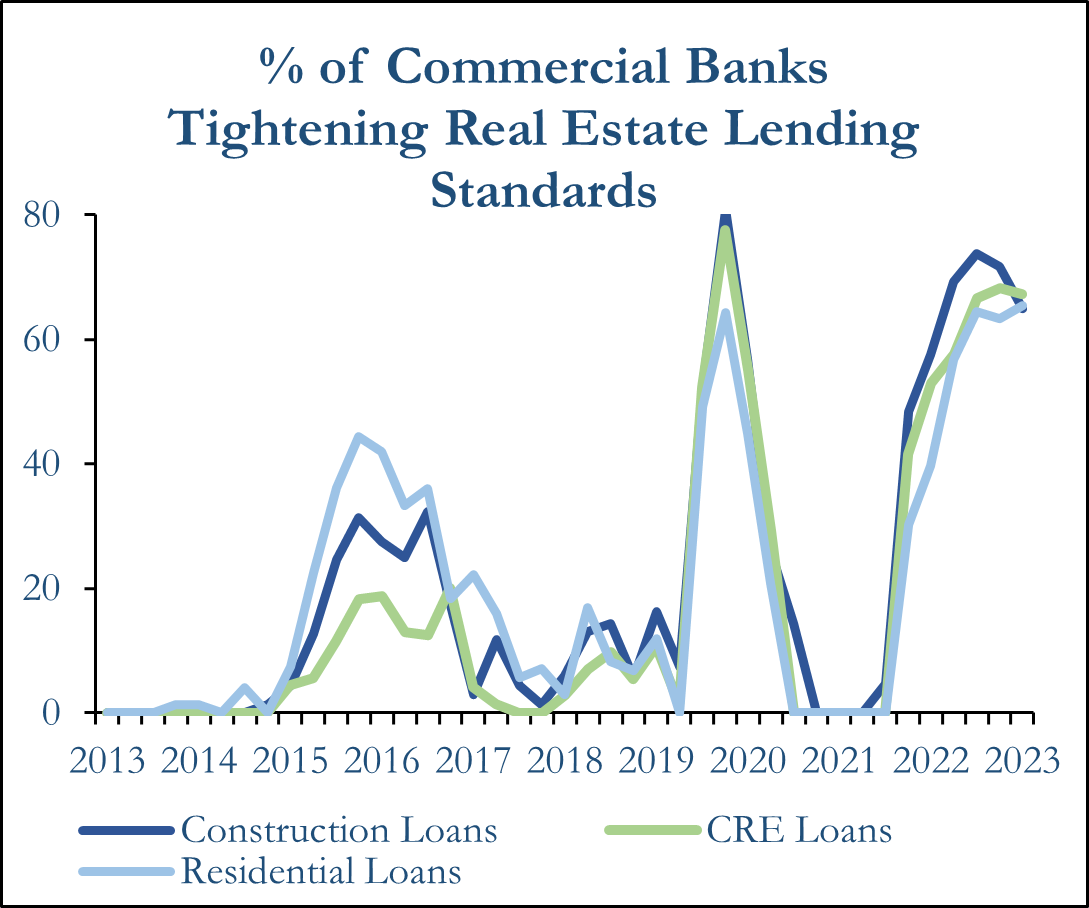

United States Commercial Banks have significantly tightened their lending standards for new commercial real estate loans. Source: MBA Senior Loan Officer Opinion Survey

The Federal Funds Rate reached 5.25%-5.50% in July 2023. Source: FRED

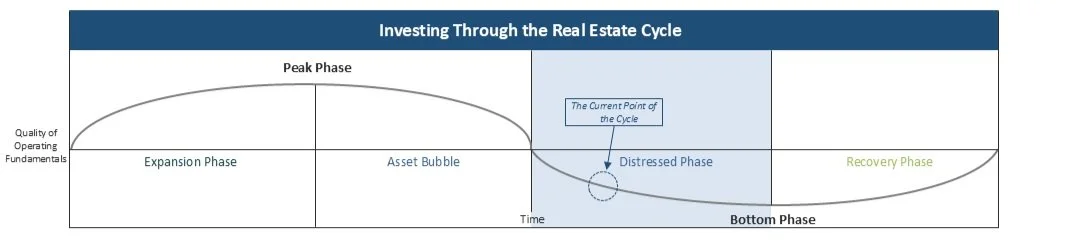

The environment today is also supported by the current point in the real estate cycle. ORG believes that the real estate cycle is past the asset bubble period and has entered into a distressed period. Aside from the office sector, today’s real estate “distress” has not generally resulted from poor operating fundamentals as in previous cycles but rather from the dislocation of the capital markets.

The rapid increase in interest rates has been the primary contributor to the recent declines in asset values and has in turn presented the opportunity for real estate investors to provide preferred equity financing on performing multifamily assets with challenged capital structures. This strategy could allow investors to achieve equity-like returns in debt-like positions.

Qualities of Multifamily Investments – Why Now?

The current real estate and capital market environment has created an attractive point-in-time opportunity for investors with a thorough understanding of the structure, terms and underlying real estate collateral to earn asymmetrical returns in multifamily preferred equity investments.

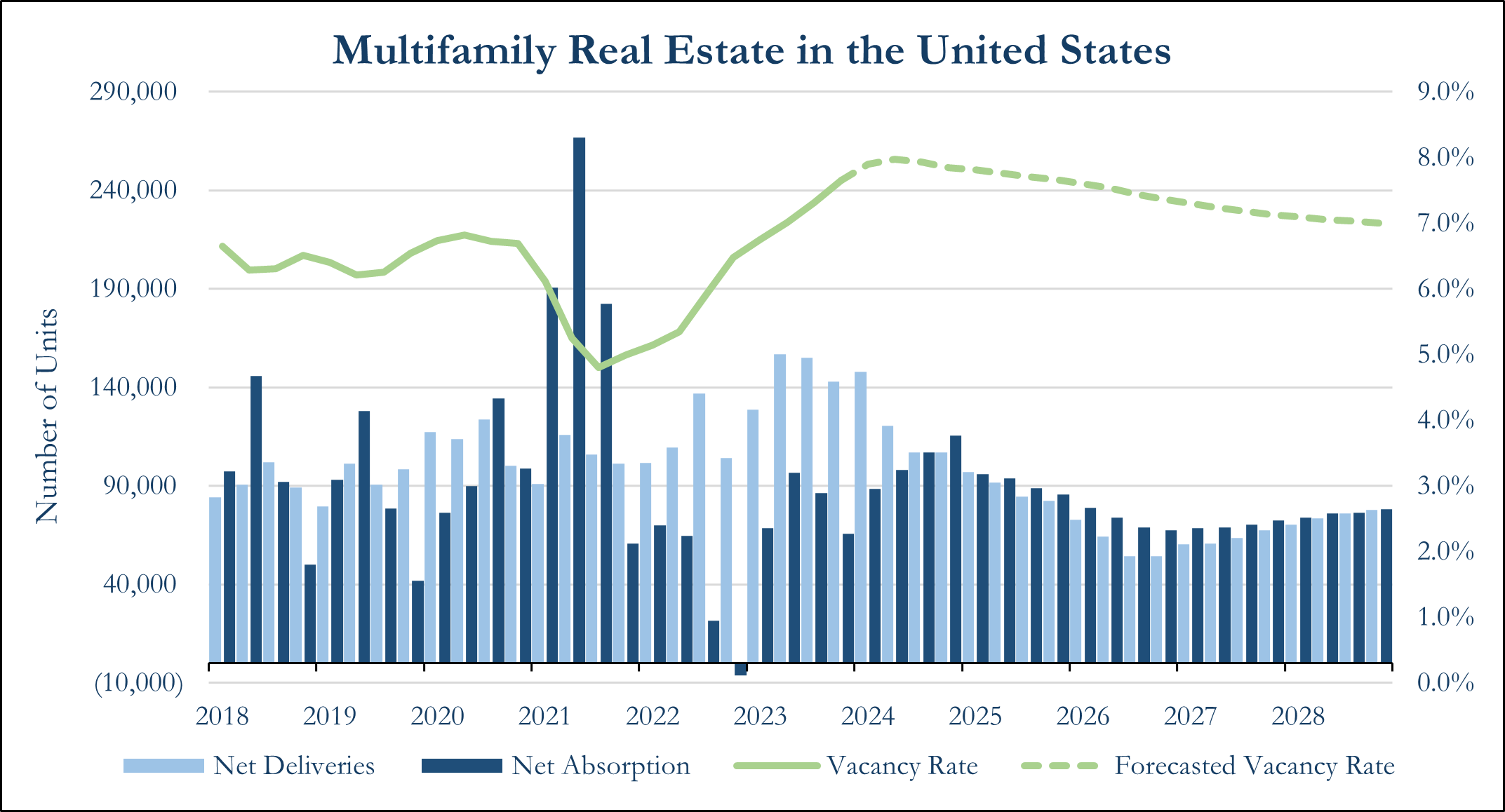

Multifamily assets have created a particularly attractive opportunity for preferred equity due to the sector’s historically resilient fundamentals and the current supply-demand imbalance. Many markets across the United States are beginning to experience an oversupply of multifamily rental units as construction projects started during periods of lower interest rates reach completion. Approximately 593,000 new units were delivered in 2023, which was the highest level since the mid-1980s, and net absorption was only 343,000 nationally. The number of units under construction peaked in the first quarter of 2023 and has since fallen with a projected 21% decrease in deliveries for 2024 [1]. Higher interest rates and construction costs are predominantly responsible for the significant decline in construction starts and thus deliveries in the coming years which is likely to cause a resurgence in rent growth for the sector as supply and demand reach an equilibrium.

The United States has seen a significant uptick in multifamily units coming online. Source: CoStar

ORG believes that the current oversupply is a temporary challenge due to a shortage of housing in the United States and an opportunity has been created to invest in assets with upside potential as supply and demand recover. The gap between available residential units and household formations rose to 2.3 million in March 2023 [2]. Furthermore, net immigration into the United States was estimated to have reached 3.3 million last year with many moving into major metropolitan areas [3]. The demand for rental units has only continued to increase as home prices have soared since the COVID-19 pandemic and many potential buyers have been priced out of the market. Due to such factors, ORG believes this to be a point-in-time opportunity to invest in multifamily as demand rebounds and the additional assets are absorbed.

Structuring Multifamily Preferred Equity Investments

The mortgage market secured by commercial income producing properties stood at $4.69 trillion as of the end of 2023 where multifamily loans represented over 44% of outstanding real estate loans [4]. As a wall of debt is coming due, multifamily borrowers will look to negotiate an extension with lenders or be required to refinance their loans. Upon refinancing, borrowers are likely to seek additional capital since proceeds from refinancing will be lower due to debt service coverage ratio (“DSCR”) requirements. With larger interest payments, borrowers are unable to meet lender requirements presenting investors with the opportunity to provide preferred equity financing to bridge the gap in the capital stack.

The market for preferred equity on multifamily assets could allow investors to earn yields of 13%-15% while achieving gross internal rates of return (“IRR”) of 17%-18%. The coupon rate on preferred equity is typically paid with a mix of current pay and accrual. Current pay acts similarly to interest paid on a traditional loan while accrual is paid in-kind at the maturity of the position or when a liquidity event occurs. In general, preferred equity is approximately paid half in current pay and half in accrual but can vary depending on terms negotiated between the lender and borrower. The additional 200-300 basis points of return are generated by fees paid on both origination and takeout. Although mezzanine debt is more attractive to borrowers due to lower rates, many lenders prohibit the use of a second mortgage and preferred equity prevails as a viable option for borrowers to access the necessary capital.

As a result of lower valuations in conjunction with DSCR and LTV requirements from senior lenders, the gap in the capital structure could arise from the 55%-75% LTV range or anywhere in between. This can allow for 25% or more of common equity subordination providing attractive downside protection for investors.

Since preferred equity is relatively costly to incur, borrowers are likely to be motivated to reduce the cost of capital by paying down the loan prior to maturity. In the event that a borrower prepays their loan, investors may achieve a stronger IRR but the overall performance of the investment will be disappointing as the resulting equity multiple will be much weaker than projected. Investors may consider mitigating such risk with the inclusion of a prepayment penalty in the loan terms.

Prepayment penalties may be structured as a lockout clause, yield maintenance and minimum multiple provision. Lockout clauses prohibit borrowers from prepaying loans for a specified period of time after origination and ensure that investors will receive predictable interest payments for the duration of the lockout. However, borrowers remain able to fully pay down loans after the lockout period expires and projected returns will not be achieved.

Yield maintenance indemnifies lenders by requiring that borrowers must pay a penalty equal to the product of the present value of the remaining cash flows less the spread over the risk-free rate [5]. Upon payment of yield maintenance, the investor has successfully protected their equity multiple and achieved an elevated IRR.

Yield Maintenance Penalty = Present Value of Future Cash Flows x (Interest Rate - Risk Free Rate)

Given the difficulty of securing yield maintenance, investors should then consider negotiating a minimum multiple provision in the loan terms. The requirement guarantees that an investor will earn a certain equity multiple and is typically agreed upon between 1.1x-1.4x. Minimum multiple provisions act as a safeguard to preserve an investor’s projected cash flow until the equity multiple is achieved.

Conclusion

ORG believes that investing in multifamily preferred equity is one of the more attractive opportunities today as investors can earn equity-like returns on debt-like investments. The current distressed period in real estate is unique because it has primarily resulted from a capital markets dislocation as opposed to a deterioration of operating fundamentals. The resulting gap in stressed capital structures is likely to warrant the need for a preferred equity piece that may yield double-digit returns with significant subordinated equity. A key factor to consider in generating strong returns is the inclusion of a prepayment penalty in the negotiated loan terms, and although yield maintenance is the most attractive to investors, the market may not allow for its inclusion. Preferred equity investors should then necessitate a minimum multiple to mitigate prepayment risk. Due to the resilient fundamentals and ability to capitalize on the supply-demand imbalance, ORG believes multifamily preferred equity to be a high conviction opportunity likely to persist through 2026.

[1] “Multi-Family National Report,” CoStar, https://product.costar.com/

[2] “The US Housing Market is Short 6.5 Million Homes,” CNN Business, https://www.cnn.com/2023/03/08/homes/housing-shortage/index.html

[3] “Immigration Drove America’s Postpandemic Urban Growth.” The Wall Street Journal, https://www.wsj.com/us-news/us-census-immigration-population-growth-cities-db007d64

[4] “Commercial and Multifamily Mortgage Debt Outstanding Increased in Fourth-Quarter 2023,” Mortgage Bankers Association, https://www.mba.org/news-and-research/newsroom/news/2024/03/14/commercial-and-multifamily-mortgage-debt-outstanding-increased-by-37-billion-in-third-quarter-2023

[5] “Yield Maintenance,” AssetsAmerica, https://assetsamerica.com/yield-maintenance/