May 16, 2022

Life Science R&D - A Deeper Dive

Introduction

Recently life science research and development (“R&D”) has been brought to the forefront of many real estate investors’ minds. The onset of the COVID-19 pandemic brought light to the necessity of advancements and improvements in drugs, medical devices and other biomedical products. As discussed in ORG’s previous Thought Piece published on November 8, 2021, “Life Science Real Estate - Where Money is Moving Fast”, venture capital funding has also accelerated in recent years. 2021 was a record year for venture funding at over $90 billion of funding, which represents approximately a 150% increase in funding from 2018. Additionally, pre-money valuations of biotech companies increased 21% year over year in 2021. This acceleration in funding has fueled more startup life science companies to launch and with more amounts of cash than ever before. With this, life science R&D lab space has become sacred with many of the top markets reaching vacancies of lower than 3%. As a follow up to ORG’s previous Thought Piece on life science, ORG wanted to provide a deep dive on R&D lab real estate.

What is Life Science R&D Lab Space?

R&D lab space provides an area for companies to conduct research and development and operate their business functions. This is much different than life science Good Manufacturing Practice (“GMP”) space which are industrial-like facilities where life science companies manufacture their products. A typical layout of R&D space consists of approximately 60% lab space and 40% office space. The building typically requires enhanced building systems and specific components in order for the tenant to conduct research and development. This includes enhanced HVAC and waste disposal systems, large floor plates with a floor load of 125-150 pounds per square foot, floor-to-ceiling heights of at least 15 feet and separate loading zones for typical shipping and receiving. Life science tenants typically require similar characteristics with the space they use which allows for R&D lab spaces to have much more reusability than typical office space.

Market Overview

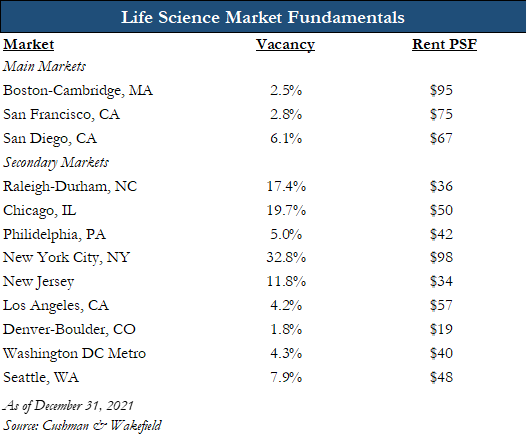

Life science companies have long been located around major research universities where talent is predominantly centered. For decades this has included three major hubs: Boston-Cambridge, MA, San Francisco, CA and San Diego, CA. However, with the recent acceleration in venture capital funding in life science, secondary markets have emerged. This mainly includes the Research Triangle which is located in the Raleigh-Durham, NC market, Chicago, IL, Philadelphia, PA, New York City and New Jersey corridor, Denver-Boulder, CO, Los Angeles, CA, Seattle WA and the Washington DC Metro.

While there are secondary markets emerging in the life science industry, there is a large difference in the fundamentals between the major and secondary markets. The three major hubs continue to show extraordinarily low vacancy rates that have driven rents to grow at record levels. The Boston-Cambridge market has experienced a 90% increase in rent over the last two years. Additionally, San Diego and San Francisco have experienced rent growth of over 50% over the last two years. However, many of the secondary markets have weaker fundamentals that raise concern for the long-term investment environment. The table below shows some of the key fundamentals by market:

Analysis of Life Science

When analyzing the investment landscape of R&D, most investors are attempting to convert traditional office buildings to R&D buildings. Converting an office building that meets the pre-specified criteria for an R&D building of large floor plates with a floor load of 125-150 pounds per square foot, floor-to-ceiling heights of at least 15 feet and separate loading zones will still require enhancement of the building’s HVAC and waste disposal systems and a complete buildout of the interior of the building to include a combination of lab and office space. The upfront costs of the conversion are high and depending on the market it costs generally $200-$300 per square foot to acquire the office building and $300-$500 per square foot to convert the building. Conversions typically take roughly 18-24 months to complete. While these upfront costs are high, this is mitigated by the reusability of the space that is created. Most life science tenants require similar lab and office space. Once the space is built there are low tenant improvement costs to release to new tenants.

The current undersupply of R&D space has led to low vacancies in the majority of markets. This supply and demand imbalance is expected to grow with the increase of funding to life science companies which creates an opportunity for investors. Investor demand for R&D properties is also expected to grow as other subsectors of office struggle in the current real estate environment.

Life science companies want to start operations quickly which means that build to suit space is not an option and investors have to develop or convert life science buildings speculatively. This exposes investors to construction and leasing risk. However, historically low vacancy levels in most markets has made these risks less of a concern for investors. R&D real estate development and conversion is currently a competitive space with considerable amounts of new supply set to come on the market soon. In addition to construction and leasing risks, investors holding life science properties are exposed to tenant credit risk due to most tenants lacking quality credit. Investors have often looked past this due to lower vacancy levels, rapid rent growth and the current supply demand imbalance. However, with higher levels of supply expected to come on the market in the next 2-3 years, tenant credit will begin to increase in importance when leasing space.

Conclusion

When looking at opportunities to invest in R&D space, investors must consider a multitude of factors such as surrounding research universities, vacancy rates, levels of demand, current and incoming supply of the market and construction costs among other factors. Experienced investors will be able to acquire high quality yet struggling office buildings that have the characteristics required for an office to lab conversion at a significant discount to replacement cost. However, there are still large risks associated with the speculative and costly conversion process. Inexperienced investors could potentially get in trouble when investing in markets with shallow demand and increasing supply or acquiring office buildings not fully capable for conversion. ORG believes there is opportunity to invest in R&D space, however manager selection is crucial. Managers must have a deep understanding of the markets, understand what office buildings require for conversion and have a strong leasing ability to stabilize the property upon completion.

Sources: Alexandria Real Estate, CBRE, Cushman & Wakefield, Green Street, Jadian Capital, Pitchbook