January 30, 2026

2026 United States Real Estate Outlook

Introduction

Going into 2025, there was high optimism from real estate market participants as the United States capital markets ecosystem began to emerge from the disruption resulting from inflation and rising interest rates throughout 2022 and 2023. This optimism was largely halted as the Liberation Day trade policy announcements in April 2025 introduced significant short-term uncertainty around capital markets and company margin compression. This caused significant fears and a scramble for real estate investors as they looked to investigate how tenant health, building materials and interest rates could be impacted as a result.

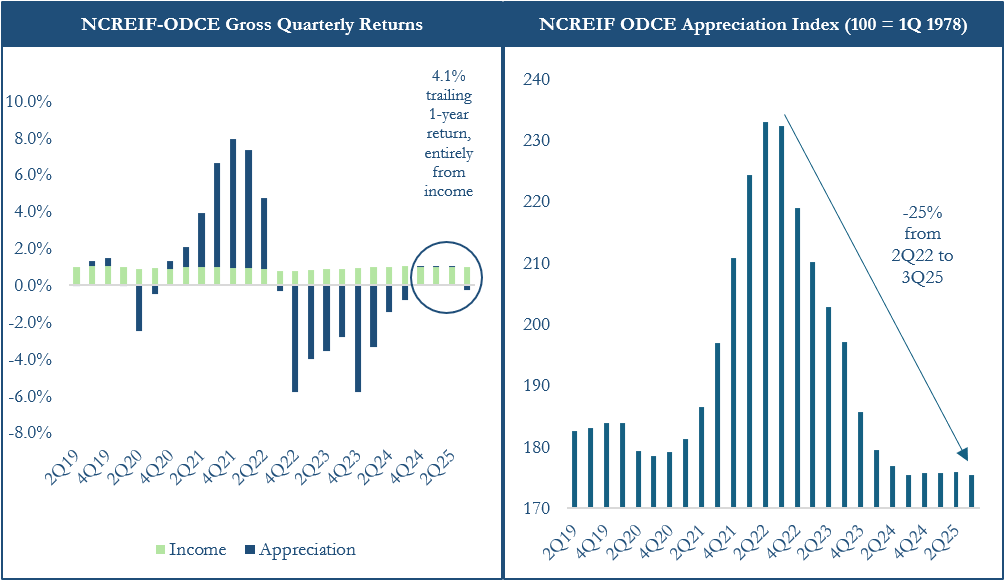

As the year progressed, the market adapted to new trade policy and elevated tariffs. However, the policies themselves became less pervasive over time as trade agreements were announced and international trade relations eased. Ultimately, tariff-related disruptions did not cause meaningful negative impacts on the real estate investment landscape in 2025 and returns remained stable with the NCREIF Open-end Diversified Core Equity (“NCREIF-ODCE”) index posting its first year of positive returns since 2022 [1].

With a positive returning quarter in 4Q 2025, the NCREIF-ODCE could post its first year of positive returns since 2022 and has rebounded 4.3% since its trough in 2Q 2024, likely indicating a stabilization in real estate values. Source: NCREIF

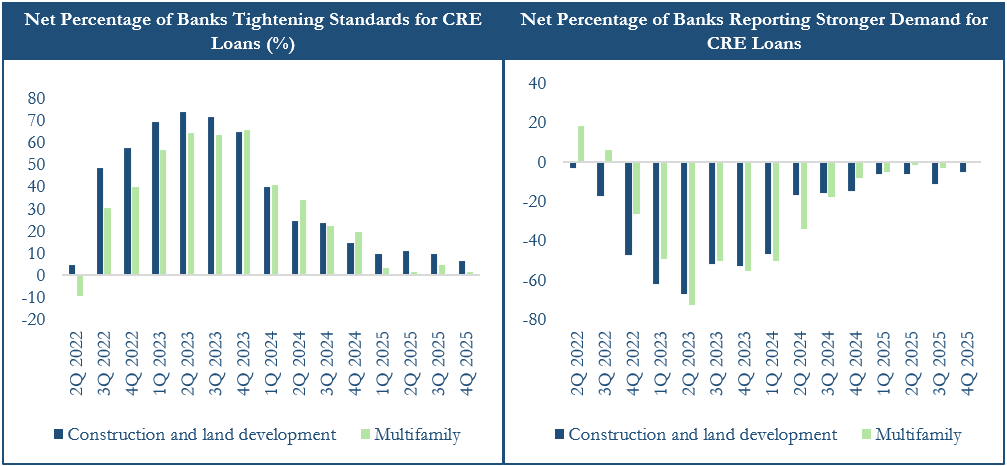

On the contrary, these disruptions created an opening for CMBS and banks to reclaim market share in real estate lending with real estate credit funds remaining active which effectively reopened debt capital markets and injected liquidity into the system.

Source: Mortgage Bankers Association, Senior Loan Officer Opinion Survey, October 2025

ORG believes that the resiliency of the capital markets and real estate fundamentals could lead to a favorable real estate investment environment in 2026. Markets are flush with debt capital at lower interest rates than those since 2023 which could cause accelerating transaction activity and refinances. Refinances have opened up a new form of exit optionality that has not existed since before 2022. This could benefit institutional real estate investors by allowing for more robust distributions from both closed-end real estate funds and open-ended core fund redemption activity. In 2026, ORG believes that in the open markets, cap rates have stabilized at a level where positive leverage can more commonly be achieved day one for new acquisitions and that un-trended stabilized yields on cost and development yields are more attractive compared to cap rates and interest rates. This could lead to a positive vintage year for new equity deployments and distributions back to investors in the real estate investment market.

Capital Markets

Interest Rates

The Federal Funds rate currently sits at a target range of 3.50% to 3.75% following 75 basis points of rate cuts during 2025 [2] and the 10-Year United States Treasury yield has decreased from approximately 4.60% in January to 4.15% by year end [3]. This compression has unlocked transaction activity with commercial mortgage coupons ranging from 5% to 6% and cap rates at slightly higher levels than interest rates as of the second half of 2025. The result has been more opportunity for acquisitions to pencil with positive leverage.

ORG expects interest rates to continue drifting lower as Federal Reserve governance becomes more dovish with the appointment of Kevin Warsh as Chairman of the Federal Reserve. Mr. Warsh has long been an intense critic of the Federal Reserve having served as a Board Governor during the Global Financial Crisis of 2008 to 2009. Prior to the Fed, Mr. Warsh had private sector experience in Morgan Stanley’s mergers and acquisitions investment banking division. His stances on interest rate policy as of late have been largely in favor of decreasing the Federal Funds Rate to spur economic growth, to increase innovation by facilitating Artificial Intelligence (“AI”) proliferation and to improve the health of the labor market.

ORG projected 50 basis points of cuts in its 2025 United States Real Estate Outlook [4], which was aligned with market expectations at the time. Ultimately, 2025 delivered 75 basis points of cuts which was a slightly dovish surprise. This mainly resulted from lower than expected inflation and growing fears of weakness in the labor market with low hiring activity [5].

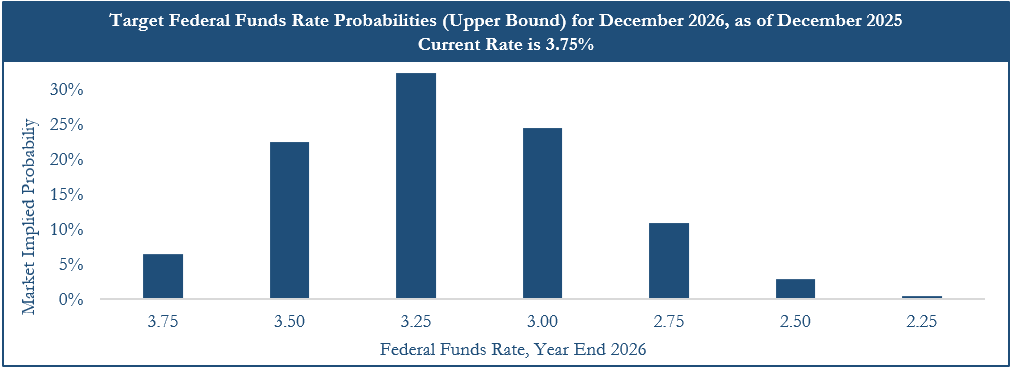

Going into 2026, the market projected 50 basis points of decreases to the Federal Funds Rate. However, ORG believes a new regime change at the Federal Reserve in the second quarter of 2026 will almost certainly lead to lower rates throughout the year.

Sources: Federal Reserve Economic Data, SEC.gov

Capital Flows

Distributions to investors remain a major pain point across the industry as both non-core and core funds slowly liquidate assets. Core funds have begun reducing queues with redemption requests as a percentage of net asset value (“NAV”) declining from approximately 15% to approximately 10% [6]. This has mainly resulted from rescinded redemption requests and modest distributions. ORG believes that open-ended core funds remain overvalued as current value cap rate marks have remained below 5% since 3Q 2014 [7] which is lower than where ORG has observed that core properties trade on the open market at approximately 5.00% to 5.25% for industrial and apartments and 5.50% to 6.25% for retail. As a result, even though buying core assets at market pricing looks attractive, open-ended core funds still remain an unattractive area to allocate new capital to due to the slow repricing of core portfolios.

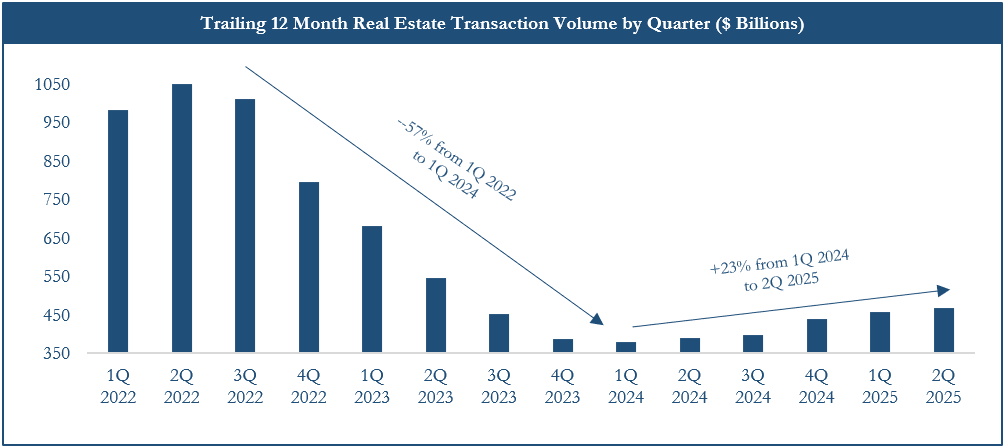

Despite this, ORG is optimistic about liquidity returning to the market through closed-end, non-core funds as values have likely stabilized and fundamentals remain strong presenting a more attractive exit environment. This stabilization could continue to drive increased transaction activity, which has been observed since 1Q 2024, particularly given that capital markets remain flush with debt capital.

Real estate transaction volumes have steadily increased since their trough in 1Q 2023 as capital markets have improved. Source: Real Capital Analytics

Source: CME Fedwatch Tool, as of December 2025

ORG has also observed that lower market interest rates have allowed for more refinance activity. For the first time since interest rates began to increase in early 2022, business plans can consider cash-out refinancings as viable liquidity options.

While transaction activity has increased and capital markets are improving, a trend in the marketplace has been that smaller assets and portfolios are experiencing significantly greater liquidity than larger assets as ORG has observed that many large assets and portfolios exceeding $100 million have become significantly harder to sell. Because of this, asset size has been critical for keeping business plans on time with approximately 86% of commercial real estate transactions over the last five years being less than $35 million in size and trading at more favorable cap rates [8]. ORG believes that at this point in the market cycle, this trend will persist throughout 2026 benefitting middle market and lower middle market investment managers and local operators.

Property Types

Retail

Following the tariff announcements in April 2025, concerns emerged surrounding retail real estate assets due to potential goods inflation and consumer weakness. Even though consumer sentiment remains low [9], these fears have not materialized in the form of inflation and the consumer remains in good health [10].

Over the past three years, retail has been the best performing property type in the NCREIF Property Index due to its resilience and attractive income returns. These characteristics make it a strong foundation for core equity portfolios and mid-to-long-term holds. ORG will continue to focus on strip centers, grocery-anchored centers and neighborhood centers as long as income returns remain robust.

Housing

ORG believes that supply needs to be looked at with nuance on a bottom-up basis. Low regulation Sun Belt markets such as Phoenix and Austin are largely oversupplied [11] while high regulation gateway markets such as New York and San Francisco remain undersupplied [12], and even within these markets, there are submarkets with their own supply and demand dynamics that deviate from market averages.

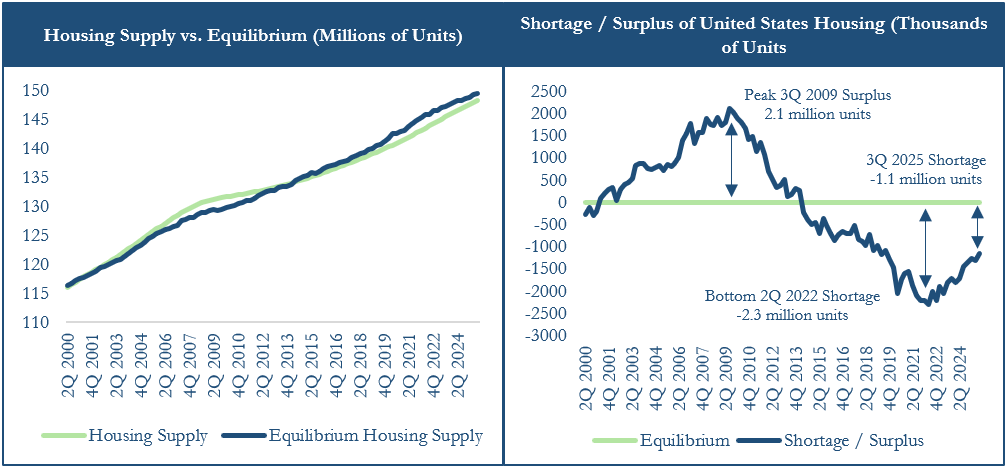

As shown by the chart below, the housing shortage has improved in recent years at the national level which should warrant critical thought from investors operating under the assumption that housing is grossly undersupplied. Additionally, longer run vacancy rates would suggest that the most exacerbated area of the national housing market is the owned housing market, where vacancy rates are 31.8% below historical averages since 2000 [13] versus 13.3% below historical averages since 2000 for rental housing as of 3Q 2025 [14]. Investors in rental housing must be aware that there is risk associated with assumptions of high rent growth, even with limited new construction starts, so it is important to ensure that housing investment strategies maintain a margin of safety. Rent growth could be strong but will be highly asset-specific. Investors should exercise caution given that going-in cap rates are lower compared to other property types.

Housing is undersupplied, but the undersupply has improved since 2022. Source: Federal Reserve Economic Data, ORG Analysis

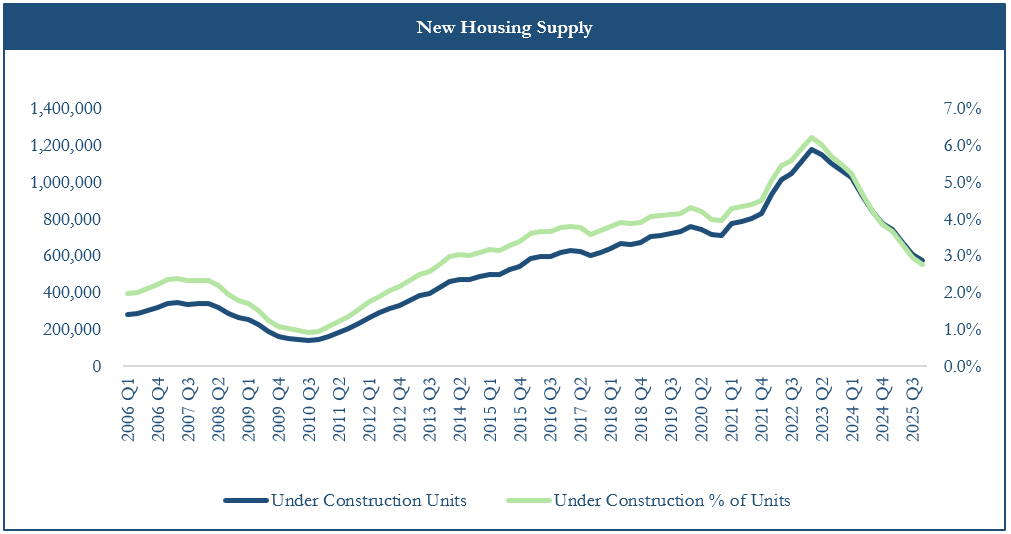

Despite this, a structural housing shortage remains in the United States which has been driven by low supply growth and is likely to continue to some degree due to limited new construction starts. This supply and demand dynamic could present investors continued opportunities to acquire assets at discounts to replacement cost. The main issue causing housing unaffordability in the United States is regulation and excess costs that constrain construction of new supply. Because it is unlikely that permitting reform will materialize in a meaningful way, ORG believes that supply and demand for this sector could be compelling for investors over the longer run.

Source: CoStar

Single family rentals and build-to rent housing has been a growing area of investor demand and interest since the beginning of the 2020s. The largest risk for the sector, particularly for scattered site strategies in which an investor may purchase individual homes on the open market, has been headline risk of institutional investors buying homes that could drive up prices for individual investors. Recently this headline risk has materialized with the United States government taking aim at institutional investors buying single family homes [15]. It remains to be seen whether this proposal becomes reality and if so, how it will materialize into American law. Regardless, ORG will closely monitor how this proposal evolves and the impact it has on single-family rental returns.

Industrial

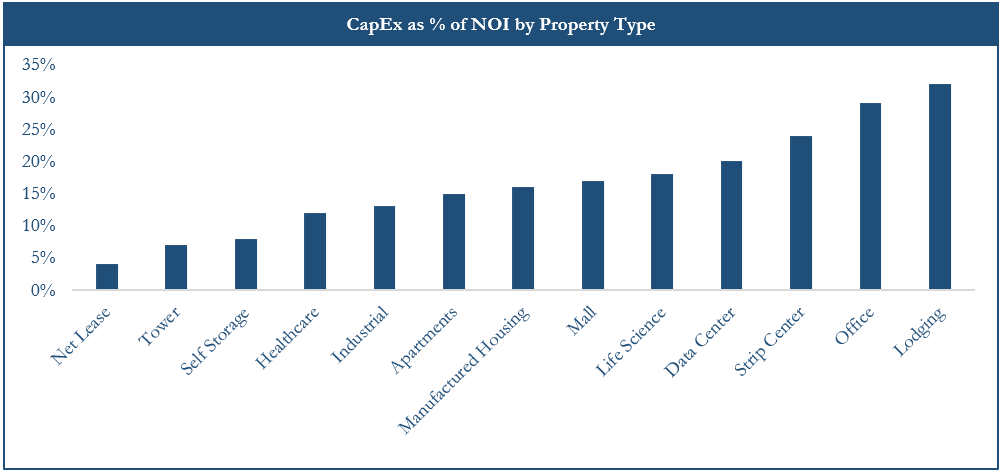

ORG believes that multi-tenanted infill industrial continues to be one of the more attractive property sectors. This stems primarily from the opportunity to mark leases to market, resilient occupancy despite tariff-related volatility and demand from logistics companies and retailers for supply chain redundancy. Additionally, cap rates for multi-tenanted infill industrial properties are higher and can deliver strong income returns on new acquisitions. Finally, industrial will retain the attractive feature of lower capital expenditure burdens and operating expense reimbursement through triple net leases which leads to more predictable net cash flow to investors.

Industrial remains one of the lowest CapEx property types, which is attractive for investment as it reduces risk. Source: Green Street

Conversely, bulk distribution center strategies involve substantially more risk and lower occupancy rates at the national level which requires a deeper understanding of submarket supply and demand to invest effectively [16]. While weakness in bulk distribution is market-and situation-specific, ORG believes that taking real estate location risk in multi-tenanted infill industrial over credit and single-tenant exposure risk in bulk distribution is more attractive and provides a greater margin of safety. For net leased bulk industrial, there is often more value in the lease itself than the property.

ORG has noticed that logistics and industrial companies are starting to recognize industrial outdoor storage (“IOS”), which are industrial areas for companies to store heavy machinery or materials that do not require climate control or protection from weather, as a critical component of their operations. This has been highlighted by the positive changes in the fundamentals over recent years such as the continued under supply, longer-lease terms, rent growth and better financing terms from lenders on IOS assets. This sector also remains heavily supply constrained due to difficulty with entitlement effectively cutting off the ability to add new supply. Although scalability may be challenging, it may be interesting for investment to the extent that investors can access the sector.

Office

Despite the market’s negative perception, traditional office fundamentals and capital markets for Class A assets surprised to the upside and ORG believes that the investment environment could continue to improve in 2026. ORG has observed more non-core funds actively pursuing office acquisitions of dislocated Class A properties with traditional re-tenanting and value-add improvement business plans. The Class A assets of gateway markets, primarily Manhattan, are likely to be the most desirable for fund investors going forward.

Lenders have also had more appetite to lend on office assets throughout 2025 with loan coupons around SOFR + 300 to 400 basis points. This lending appetite has mainly been from SASB CMBS markets and private debt funds. ORG believes that office values have likely bottomed and fundamentals are beginning to improve in the best assets. In lower quality assets, fundamentals may take longer to recover.

A trend in the office sector that has grown in feasibility and popularity from investors is office-to-residential conversions. These strategies can help to reduce the surplus of obsolete office space in urban cores and the shortage of residential units in some urban markets. Developers have been successful in transforming some office towers into apartments and condominiums with projects across cities such as New York, Washington DC, Chicago, Cleveland and Philadelphia demonstrating the viability of adaptive reuse as long as the basis is cheap enough.

The medical office market has experienced significant cap rate expansion over the past five years from approximately 5.5% in 1Q 2022 to approximately 6.8% in 2Q 2025 [17] as a result of higher interest rates and association with the fears in traditional office. Despite this, fundamentals and occupancy have remained incredibly resilient. The medical office market could be an attractive place to invest because of the aforementioned fundamentals, as well as NNN leases and cheap debt available from balance sheet lenders, creating one of the largest positive leverage spreads in real estate equity today. ORG will continue evaluating opportunities in this space to access high income returns.

Data Centers

Data centers remain a popular discussion topic in institutional real estate allocation decisions, though interest has slowed as concerns around AI have grown. ORG will continue to remain cautious and monitor hyperscaler demand and lease structures to ensure that tenants continue to pay rent in the event of going dark in the event of technological disruption. For this reason and the rapid evolution of the capability of novel graphics processing units (also known as GPUs), ORG believes that it could be prudent to underwrite residual value conservatively or assume no residual whatsoever on data center investments.

From ORG’s market observations, "powered land" strategies can produce very high returns but are highly speculative. Many successful deals with the business plan of obtaining power access at an owned land parcel resulted from situations in which an industrial development site had excess power supply prior to ChatGPT’s release in late 2022. This presented land owners with the opportunity to sell their parcels to hypers-scalers and data center developers at a significant premium. This will be challenging to repeat long term as by now the “secret” of power being the main driver of AI and data center activity has been discovered by the market.

Investment Structures

Risk and Return

ORG will continue to reiterate that the role of real estate in most institutional real estate portfolios is to generate income, hedge inflation and mitigate volatility by producing uncorrelated returns. As a result, with new commitments, ORG will pursue a barbell approach by focusing on strategies that have resilient and high income returns, as well as appreciation from value add strategies. Falling interest rates and positive leverage on new deals have led to non-core business plans becoming more viable, however investors should understand that returns for these strategies will likely be lower returning than the levels seen throughout the 2010s since cap rate compression will be less of a factor.

Co-Investments

Co-investments will remain a significant focus area where nimble institutions and discretionary portfolios can target dislocation, increase exposure to high-conviction assets and reduce gross-to-net fee spreads. These opportunities continue to exist due to the challenging capital raising environment for funds sponsored by investment managers. Throughout 2025, ORG has observed attractive co-investment deal flow in preferred equity, common equity, general partner carry buyouts and operating companies. Going forward, ORG anticipates seeing fewer dislocated opportunities and more growth-focused business plans including operating companies, portfolio aggregation strategies, redevelopments and ground-up developments.

Real Estate Credit

ORG continues to hold the belief that real estate credit has a unique value proposition for investors. By investing in real estate credit strategies, the investor trades off appreciation returns for high income returns with consistent cash flows and equity subordination. Additionally, ORG believes that private credit plays an important role in the real estate ecosystem and will be better for the economy as long-term risk taking capital is invested in new mortgages. This capital base is more suitable for real estate lending when compared with the regional banking system, which will always grapple with the inherent mismatch of short- term deposits and longer-term loans.

Despite increasing competition, real estate credit funds have generated resilient returns and continue to find strong deal flow. These funds compete effectively with balance sheet lenders by accessing fund-level leverage also known as back leverage through repurchase (“repo”) facilities and note-on-note financing. The reason for the significant availability in real estate credit fund back leverage capital is due to its favorable capital treatment for banks, in which real estate exposure can be classified as a security instead of as traditional real estate loans [18] leading to less regulatory scrutiny for banks. While regional banks are becoming more active in direct real estate lending [19], because of favorable capital treatment, larger banks generally prefer to get real estate exposure through providing back leverage rather than direct lending.

Most fund-level leverage arrangements feature relatively light covenants, with lines being predominantly mark-to-credit, meaning that margin calls are only allowable if there are impairments at the asset level, such as high increases in vacancy or declines in NOI. ORG believes this trend warrants continued monitoring to see if real estate credit managers begin to become amenable to capital markets-based mark-to-market provisions for higher advance rates and lower spreads. In the event of that trend materializing, then real estate credit presents considerably more risk to investors. Real estate CLO issuances have also been an increasingly popular method of financing for real estate credit funds, although not nearly as popular as repo facilities and note-on-note structures. Generally speaking, ORG believes that note-on-note financing presents less risk to real estate credit funds than repo facilities.

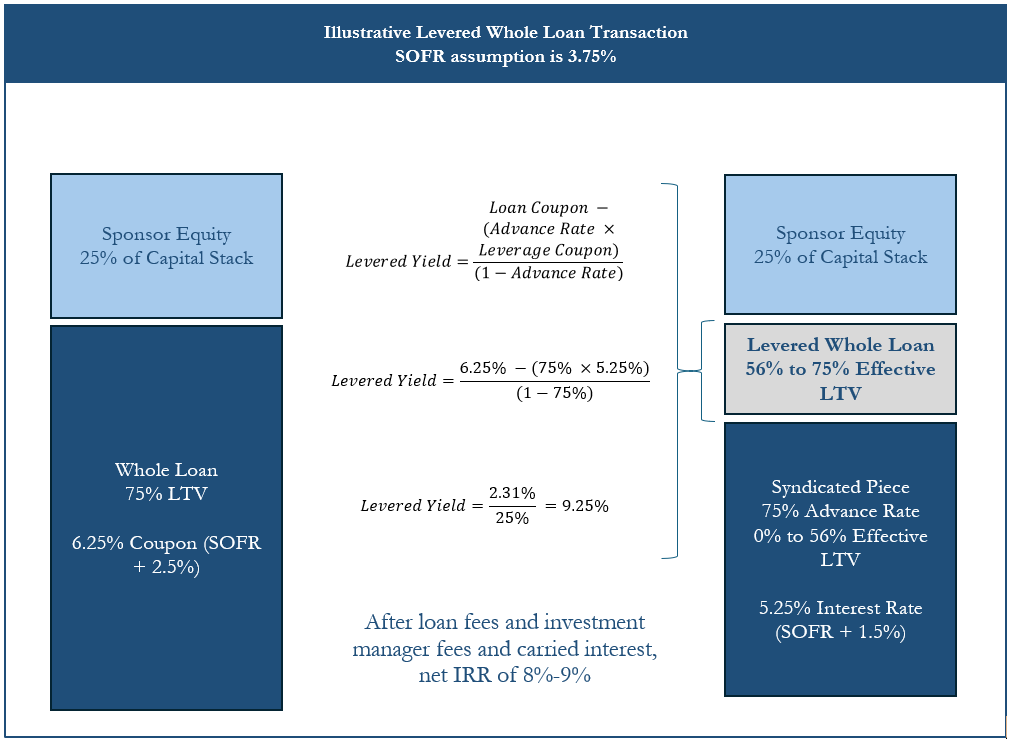

Depending on the fund structure and strategy, advance rates on real estate credit fund back leverage range from 2-to-1 to 4-to-1 with asset level loan to value ratios of 60% to 75%. Spreads for this back leverage can be as low as 125 to 150 basis points over SOFR. These funds have generally continued to generate levered yields of approximately 9% to 10% which would reflect an 8% to 9% net internal rate of return to fund investors.

Source: ORG Analysis and Market Observations

Real Estate as an Asset Class in the Broader Portfolio

In 2026, ORG believes that the case for capital deployments into non-core real estate has improved since the capital markets disruption of 2022 as institutional portfolios look beyond the peak-valuation cycles of other equity asset classes. The real estate market, particularly for housing, and some areas of industrial and retail in the United States, is characterized by shortages of new supply and high replacement costs to deliver new supply [20]. Between the supply issue, higher cap rates and some stress with forced sellers as a result of maturing loans and lenders taking back assets [21], 2026 could present an attractive entry point for new investment.

Over the last three years, investors have rightly been nervous about adding to real estate allocations due to poor performance in comparison to other private and public assets, negative leverage on new acquisitions and denominator effects. In 2026, ORG continues to see lower enthusiasm for real estate among institutional investors, however, this may begin to turn during the year. Some institutional allocators have begun to realize that fundamentals have improved for new investment into real estate. As a result, allocators continue to increase their forecasts for long run returns in non-core real estate to levels that are competitive other asset classes in the portfolio [22][23].

Conclusion

ORG believes that many signs point to 2026 being a strong year for the real estate market. Debt capital markets being flush with capital could help to facilitate transactions and refinance activity going forward. This could provide a better market for dry powder to be deployed and for existing investors to receive distributions. If distributions increase, many institutional investors will have the equity and portfolio allocation capacity to reinvest into the asset class.

Broadly real estate fundamentals remain strong, especially in retail, industrial and housing, with office markets seeing increasing levels of investor interest. Cap rates also currently sit at levels which are high enough to create positive leverage scenarios for real estate investors in the future. This could facilitate favorable acquisition environments for new capital in core and non-core investments alike.

[1] NFI ODCE Quarterly Detail Report, October 30, 2025

[2] Federal Reserve Economic Data, Federal Funds Rate Target Range, Upper Limit, as of January 2026

[3] CNBC, U.S. 10 Year Treasury

[4] Stephen Stuckwisch, et al. ORG Portfolio Management, February 3, 2025, ORG Portfolio Management – 2025 United States Real Estate Outlook. https://www.orgpm.com/research/2025-us-real-estate-outlook

[5] Howard Schneider, Reuters, October 14, 2025, Fed’s Powell says economy may be on firmer footing, but job market weak. https://www.reuters.com/business/feds-powell-says-economy-firmer-footing-though-low-hiring-low-firing-trend-2025-10-14/

[6] CRE Analyst, October 1, 2024, Core Fund Redemption Queues Remain Elevated in 2025. https://www.creanalyst.com/insights/core-fund-redemption-queues-remain-elevated-in-2025

[7] NCREIF Property Index Trends Report, 3Q 2025

[8] CoStar

[9] Federal Reserve Economic Data, Consumer Sentiment

[10] Rees Hagler and Dhiren Patki, Federal Reserve Bank of Boston, August 13, 2025, Why Has Consumer Spending Remained So Resilient? Evidence from Credit Card Data https://www.bostonfed.org/publications/current-policy-perspectives/2025/why-has-consumer-spending-remained-resilient.aspx

[11] ORG Analysis of CoStar absorption and vacancy rate data.

[12] Id.

[13] Federal Reserve Economic Data, Rental Vacancy Rate in the United States

[14] Federal Reserve Economic Data, Homeowner Vacancy Rate in the United States

[15] Craig Karmin et. al., Wall Street Journal, January 7, 2026, Trump Moves to Ban Big Investors From Buying Single-Family Homes https://www.wsj.com/economy/housing/trump-housing-large-investor-single-family-home-ban-13e06f61?mod=Searchresults&pos=3&page=1

[16] Matthew Antonis, Friend Commercial Real Estate, December 12, 2025, Small-Bay Vs. Big-Box: Where Is The True Demand For Industrial Space In 2026?

https://www.mantoniscre.com/blog/small-bay-vs-big-box-where-is-the-true-demand-for-industrial-space-in-2026

[17] Sandy Romero, Cushman & Wakefield, 2025, Medical Outpatient Buildings Capital Markets Mid-Year 2025 Update. https://www.cushmanwakefield.com/en/united-states/insights/healthcare-capital-markets-outlook

[18] Stephen Stuckwisch, et al. ORG Portfolio Management, August 1, 2024, Mortgage Loan Repurchase Facilities – What Investors Should Know. https://www.orgpm.com/research/mortgage-loan-repurchase-facilities

[19] Mark Heschmeyer, CoStar, January 20, 2026, Regional banks went quiet on commercial property loans. They’re turning up the volume again. https://www.costar.com/article/213919897/regional-banks-went-quiet-on-commercial-property-loans-theyre-turning-up-the-volume-again

[20] Tony Charles, Morgan Stanley Real Estate Investing, January 29, 2026, Real Estate at an Inflection Point, https://www.eatonvance.com/insights/articles/real-estate-at-an-inflection-point.html

[21] Trepp, January 6th, 2026, Trepp’s 2026 Predictions: A Sorting Year for Commercial Real Estate, https://www.trepp.com/trepptalk/trepps-2026-predictions-a-sorting-year-for-commercial-real-estate

[22] PGIM 2026 Capital Market Assumptions

[23] George Gatch, JP Morgan, 2026 Long Term Capital Market Assumptions